NO.PZ2023091701000061

问题如下:

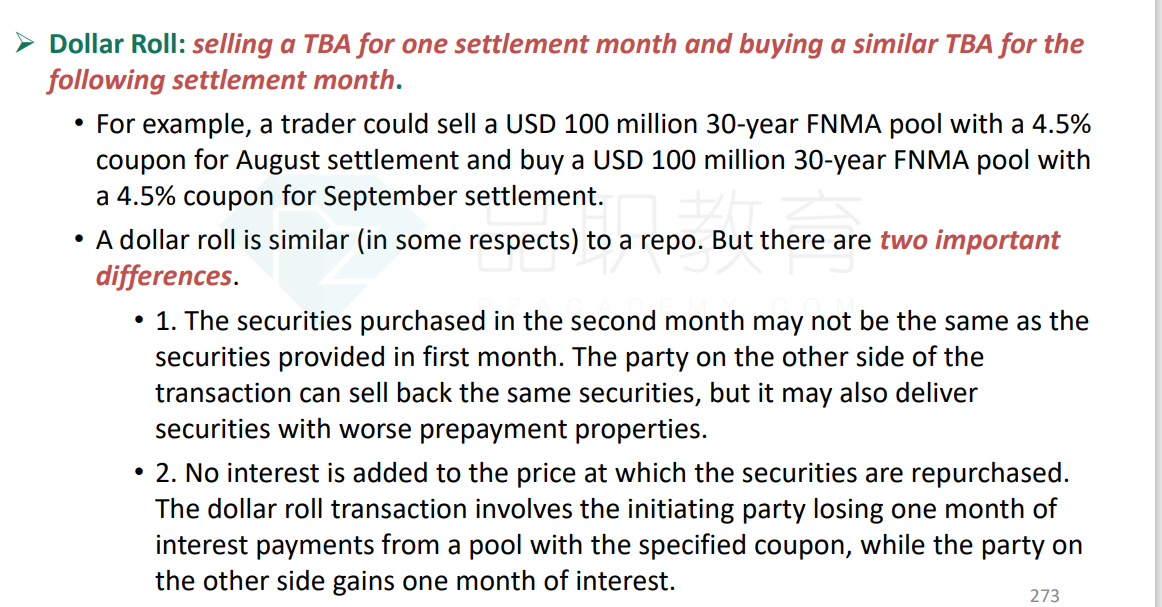

Consider an investor who wants to finance the purchase of a mortgage pool over a one month period. One alternative is to sell an MBS repo, in which case the investor could sell the pool today while simultaneously agreeing to repurchase it after a month. This trade has the same economics as a secured loan: the investor effectively borrows cash today by posting the pool as collateral, and upon paying back the loan with interest after a month, retrieves the collateral. An alternative is the “dollar roll”. In the dollar roll, the buyer of the roll sells a TBA for one settlement month (the “earlier month”) and buys the same TBA for the following settlement month (the “later month”).

For example, the investor who just purchased a 30-year 4% FNMA pool might sell the FNMA 30-year 4% January TBA and buy the FNMA 30-year 4% February TBA. Delivering the pool just purchased through the sale of the January TBA, which raises cash, and purchasing a pool through the February TBA, which returns cash, is very close to the economics of a secured loan.

But there are two important differences between dollar roll and repo financing:

I. The buyer of the roll may not get back in the later month the same pool delivered in the earlier month. The buyer of the roll delivers a particular pool, for example, in January but will have to accept whatever eligible pool is delivered in the next February. By contrast, an MBS repo seller is always returned the same pool that was originally posted as collateral.

II.The buyer of the roll does not receive any interest or principal payments from the pool over the roll. For example, the buyer of the Jan/Feb roll, who delivers the pool in January, does not receive the January payments of interest and principal. By contrast, a repo seller receives any payments of interest and principal over the life of the repo. While the prices of TBA contracts reflect the timing of payments, so that the buyer of a roll does not, in any sense, lose a month of payments relative to a repo seller, the risks of the two transactions are different. The buyer of a roll does not have any exposure to prepayments over the month being higher or lower than what had been implied by TBA prices while the repo seller does.

Which of these two differences is (are) correct?

选项:

A.Neither is correct. B.I is true but II is incorrect. C.I is incorrect but II is true. D.Both are correct.解释:

Both are correct.