NO.PZ2023091701000174

问题如下:

A risk manager at a fixed-income hedge fund wants to hedge the interest rate risk exposure of a portfolio. The manager has determined that a 1-bp increase in the 2-year spot rate would decrease the value of the portfolio by INR 1,600, however a 1-bp increase in the 5-year spot rate would increase the value of the portfolio by INR 3,450. The manager plans to hedge the portfolio’s exposure using the following two bonds whose key rate 01s (KR01s) are shown below:

Which of the following transactions would most effectively hedge against the portfolio’s interest rate risk?

选项:

A.Buy 38 of Bond A and short 56 of Bond B B.Buy 75 of Bond A and short 29 of Bond B C.Short 38 of Bond A and buy 56 of Bond B D.Short 75 of Bond A and buy 29 of Bond B解释:

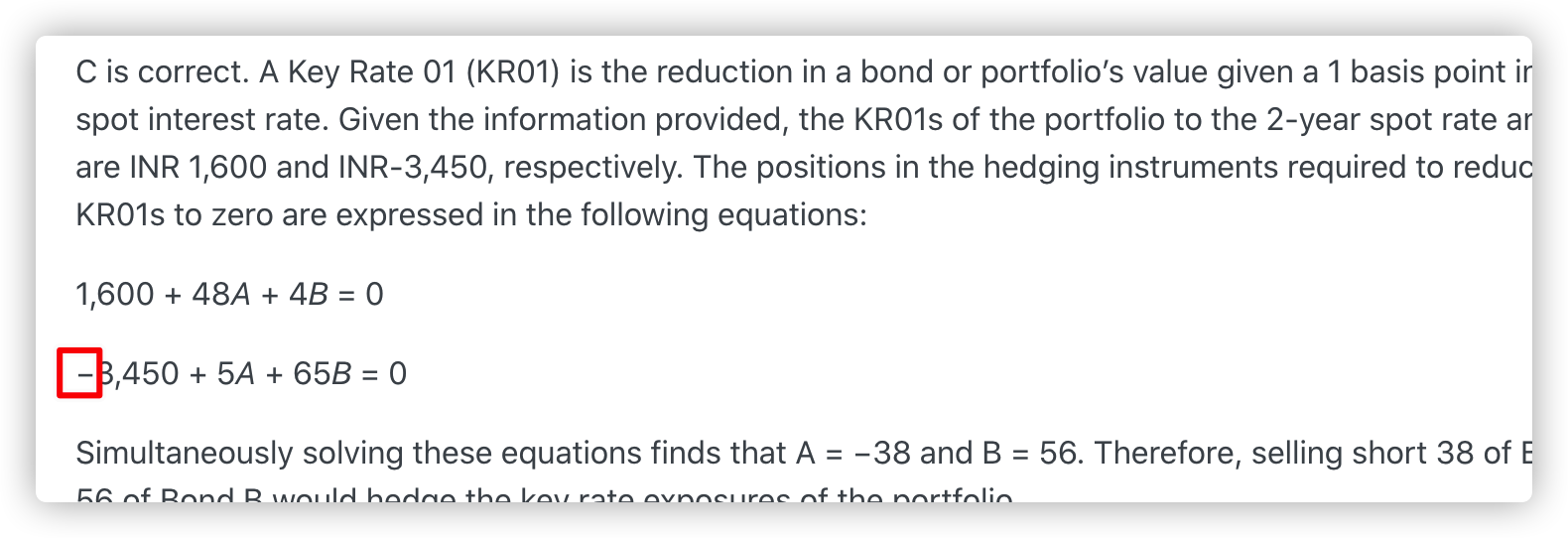

C is correct. A Key Rate 01 (KR01) is the reduction in a bond or portfolio’s value given a 1 basis point increase in a given spot interest rate. Given the information provided, the KR01s of the portfolio to the 2-year spot rate and 5-year spot rate are INR 1,600 and INR-3,450, respectively. The positions in the hedging instruments required to reduce the portfolio KR01s to zero are expressed in the following equations:

1,600 + 48A + 4B = 0

−3,450 + 5A + 65B = 0

Simultaneously solving these equations finds that A = −38 and B = 56. Therefore, selling short 38 of Bond A and buying 56 of Bond B would hedge the key rate exposures of the portfolio.

A is incorrect. This reverses the direction of the trades in Bond A and Bond B.

B is incorrect. This is the result found when the equations are set up incorrectly as:

−3,450 + 48A + 5B = 0

1,600 + 4A + 65B = 0

D is incorrect. This reverses the direction of the trades in Bond A and Bond B after the equations are set up incorrectly as in B above.