NO.PZ2023041003000039

问题如下:

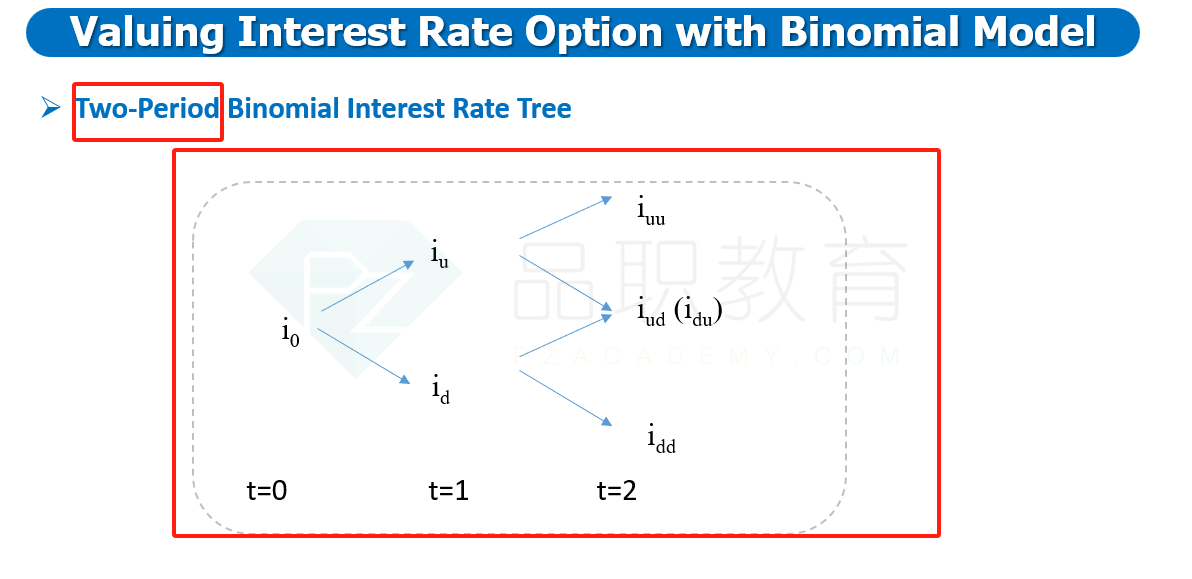

The final option valuation task involves an

interest rate option. Sousa must value a two-year, European-style call option

on a one-year spot rate. The notional value of the option is 1 million, and the

exercise rate is 2.75%. The risk-neutral probability of an up move is 0.50. The

current and expected one-year interest rates are shown in Exhibit 2, along with the values of a one-year

zero-coupon bond of 1 notional value for each interest rate.

Based on Exhibit 2 and the parameters used by

Sousa, the value of the interest rate option is closest to:

选项:

A.5,251.

6,236.

6,429.

解释:

Using the expectations approach, per 1 of

notional value, the values of the call option at Time Step 2 are

c++ = Max(0,5++ - X) =

Max(0,0.050 - 0.0275) = 0.0225.

c+- = Max(0,5+- - X) = Max(0,0.030 - 0.0275) = 0.0025.

c-- = Max(0,5-- - X) =

Max(0,0.010 - 0.0275) = 0.

At Time Step 1, the call values are

c+ = PV[nc++

+ (1 - π)c+-].

c+=

0.961538[0.50(0.0225) + (1 - 0.50)(0.0025)] = 0.012019.

c- = PV[nc+- + (1 - π)c--].

c- = 0.980392[0.50(0.0025) + (1 -

0.50)(0)] = 0.001225.

At Time Step 0, the call option value is

c = PV[πc+ + (1 -

π)c-].

c = 0.970874[0.50(0.012019) + (1 -

0.50)(0.001225)] = 0.006429.

The value of the call option is this amount

multiplied by the notional value, or 0.006429 x 1,000,000 = 6,429.

请问题干说2年,也就是2期的二叉树,为何要用到第三期的节点利率呢?