NO.PZ2023091901000076

问题如下:

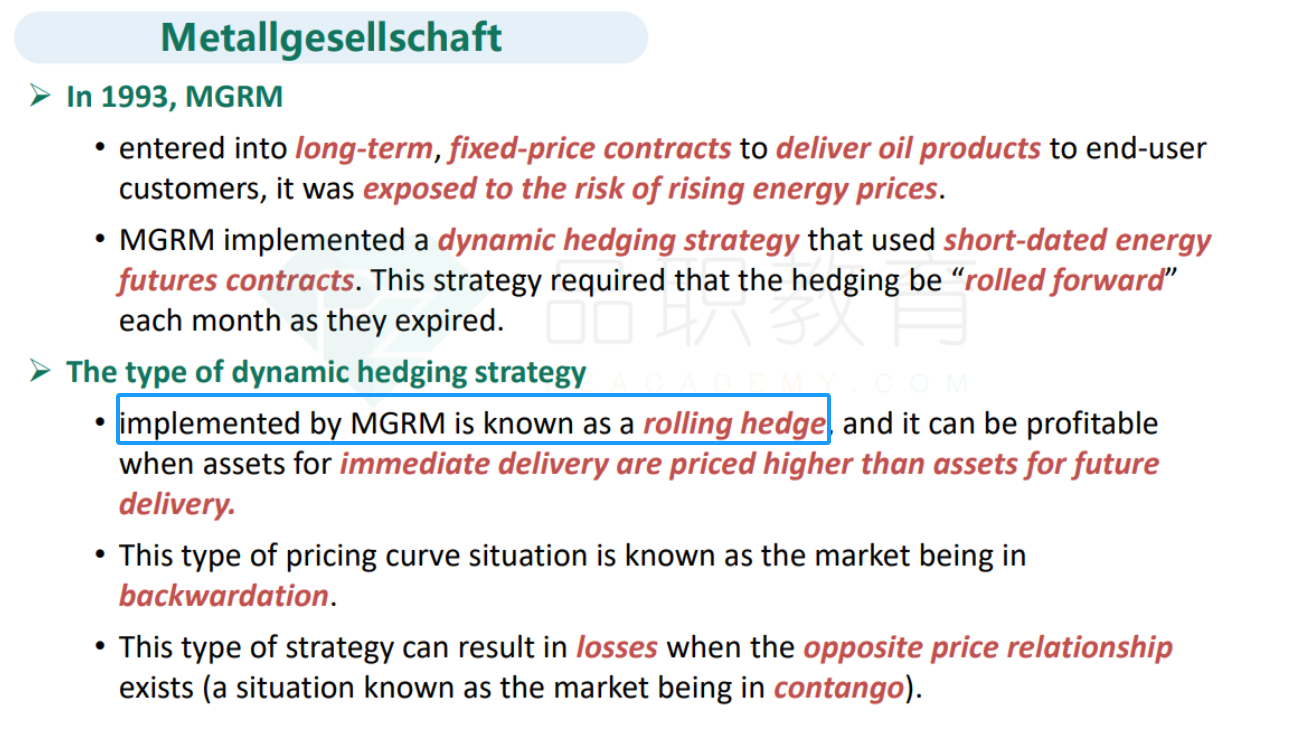

In late 1993, Metallgesellschaft reported losses of

approximately USD 1.5 billion in connection with the implementation of a

hedging strategy in the oil futures market. In 1992, the company had begun a

new strategy to sell petroleum to independent retailers, on a monthly basis, at

fixed prices above the prevailing market price for periods of up to 5 and even

10 years. At the same time, Metallgesellschaft implemented a hedging strategy

using a large number of short-term derivative contracts such as swaps and

futures on crude oil, heating oil, and gasoline on several exchanges and markets.

Its approach was to buy on the derivatives market exposure to one barrel of oil

for each barrel it had committed to deliver. Because of its choice of a hedge

ratio, the company suffered significant losses with its hedging strategy when

oil market conditions abruptly changed to:

选项:

A.Contango, which occurs when the futures price is above the spot price.

Contango, which occurs when the futures price is below the spot price.

Normal backwardation, which occurs when the futures price is above the spot price.

Normal backwardation, which occurs when the futures price is below the spot price.

解释:

Oil prices fell in the fall of 1993 because of OPEC’s

problems adhering to its production quotas, so the market changed into one of

contango, so C and D are incorrect. In contango, the futures price is above the

spot price and as a result Metallgesellchaft incurred losses on its short-dated

long futures contracts, so B is incorrect and A is correct.

M公司一开始担心价格下跌,所以搞了个short postion,但后来变成Contango了,所以就亏了