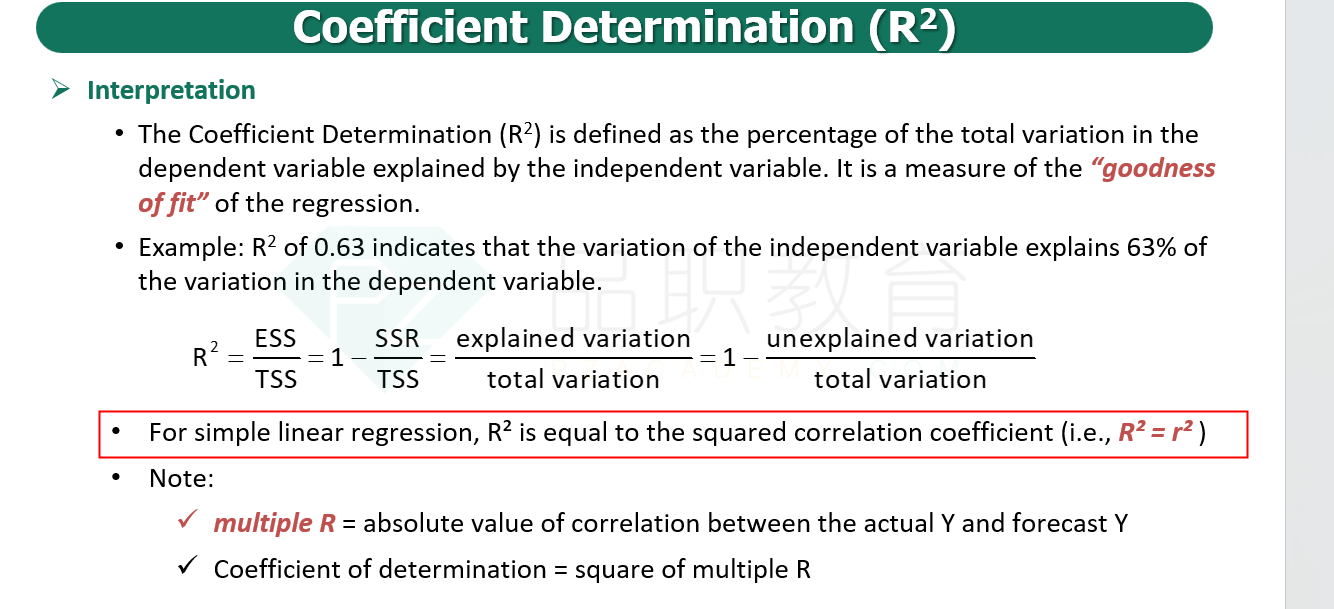

NO.PZ2019040801000076

问题如下:

An analyst gathers the following data for a regression of the annual sales for Company Bridge, a maker of oil products, on oil product industry sales.

The regression was based on six observations and the correlation between company and industry sales is 0.9126.

Which of the following is closest to the value and is the most likely interpretation of the R^2 ? The R^2 is:

选项:

A.

0.1672, indicating that the variability of industry sales explains about 16.72% of the variability of company sales.

B.

0.1672, indicating that the variability of company sales explains about 16.72% of the variability of industry sales.

C.

0.8328, indicating that the variability of oil industry sales explains about 83.28% of the variability of company sales.

D.

0.8328, indicating that the variability of company sales explains about 83.28% of the variability of oil industry sales.

解释:

C is correct.

考点:Linear Regression with One Regressor

解析:R^2 = 0.9126^2 =0.8328

自变量的变动可以解释R^2比例的因变量的变动。因此本题选C;答案D说反了。

题目中 描述 The correlation between company sales and industry=0.9**, 此处考察 multiple r = r^2 以及r^2 的解释。 multiple r 是 correlation between actual y & forecast y. 感觉的题目描述有问题