NO.PZ202403051000000301

问题如下:

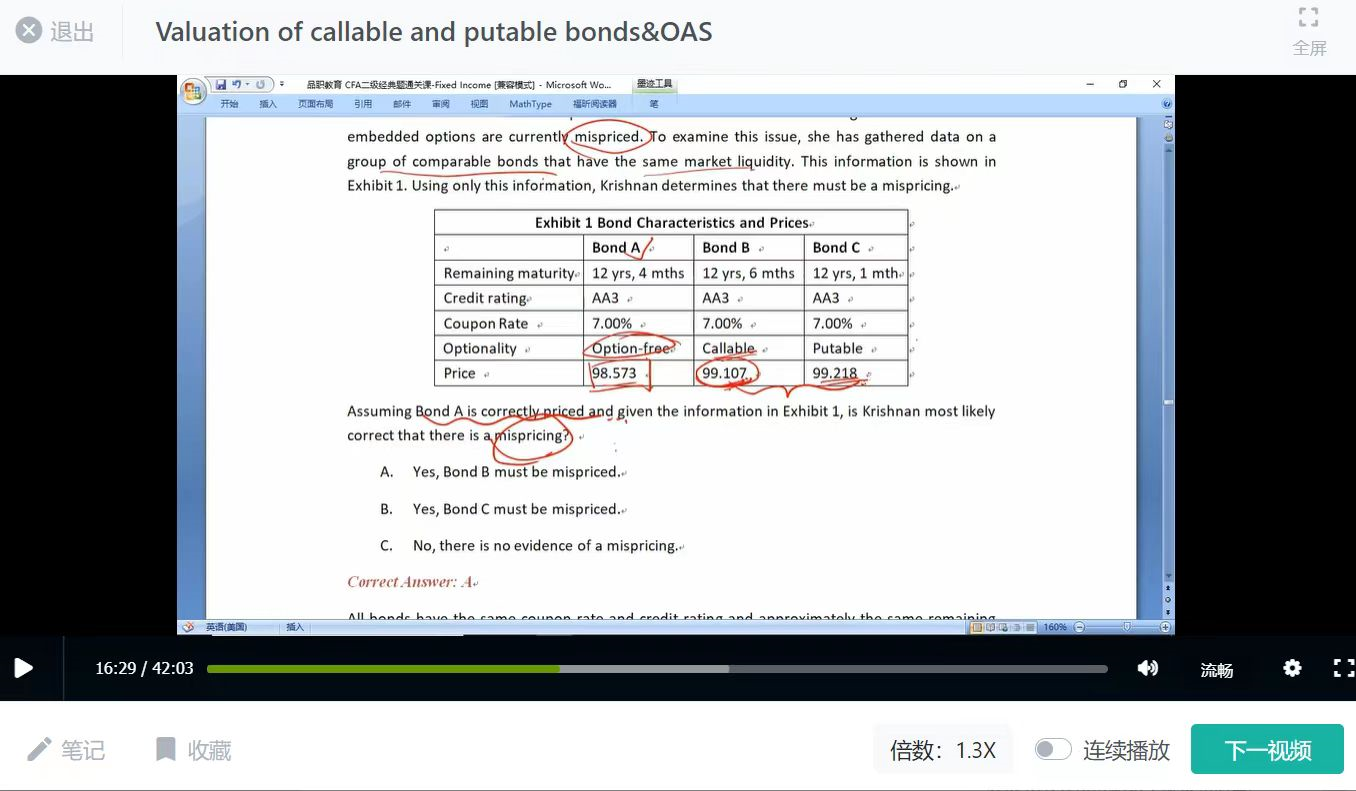

Assuming Bond A is correctly priced and given the information in Exhibit 1, is Krishnan most likely correct that there is a mispricing?

选项:

A.Yes, Bond C must be mispriced.

Yes, Bond B must be mispriced.

No, there is no evidence of a mispricing.

解释:

B is correct. All bonds have the same coupon rate and credit rating and approximately the same remaining maturity. The pricing of all three (below par), implies the coupon rate of a par bond with this credit rating and approximate maturity is higher than 7.0%. Bond A is not callable, while Bond B is callable and has a slightly longer maturity than Bond A. Both of these differences imply that Bond B’s price should be lower than Bond A’s, but it is higher.

A is incorrect because Bond A is option-free while Bond C is putable and has a slightly shorter maturity than Bond A. Both of the ways Bond C differs from Bond A would imply a higher price than Bond A, which it has. Therefore there is no evidence that Bond C is mispriced.

C is incorrect because either Bond A or Bond B must be mispriced, or possibly both.

没看懂解析“The pricing of all three (below par), implies the coupon rate of a par bond with this credit rating and approximate maturity is higher than 7.0%. Bond A is not callable, while Bond B is callable and has a slightly longer maturity than Bond A.”

然后文中说到从之前flat 到upward sloping, 那不是说利率上涨,那callable bond B maturity不是应该更短?