NO.PZ202403050900000805

问题如下:

Assuming one option per share, an appropriate delta hedge for the GI stock would most likely be to:

选项:

A.buy 40,100 puts.

B.sell 148,428 calls.

C.sell 168,010 calls.

解释:

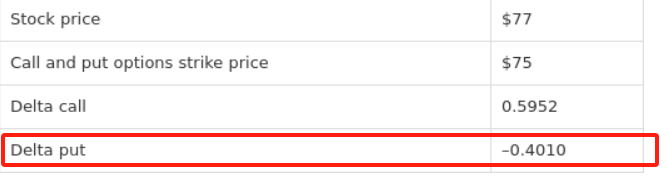

C Correct. The call delta is 0.5952. The number of calls to hedge 100,000 shares is calculated as 1/0.5952 = 168,010. An appropriate hedge for 100,000 shares of stock with a delta of 1 would be to sell 168,010 calls.

防止股价下跌不是用put option和stock组合对冲吗,为什么是用call option呢