NO.PZ2024021802000004

问题如下:

Describing ESG performance attribution at a portfolio level is difficult because:选项:

A.there is a lack of third-party data providers. B.there is a size bias in ESG ratings in favor of large companies. C.many third-party data providers describe ESG attributes as an uncorrelated, statistically independent factor.解释:

A. Incorrect because third-party data providers are developing increasingly sophisticated ESG ratings and scoring methodologies.

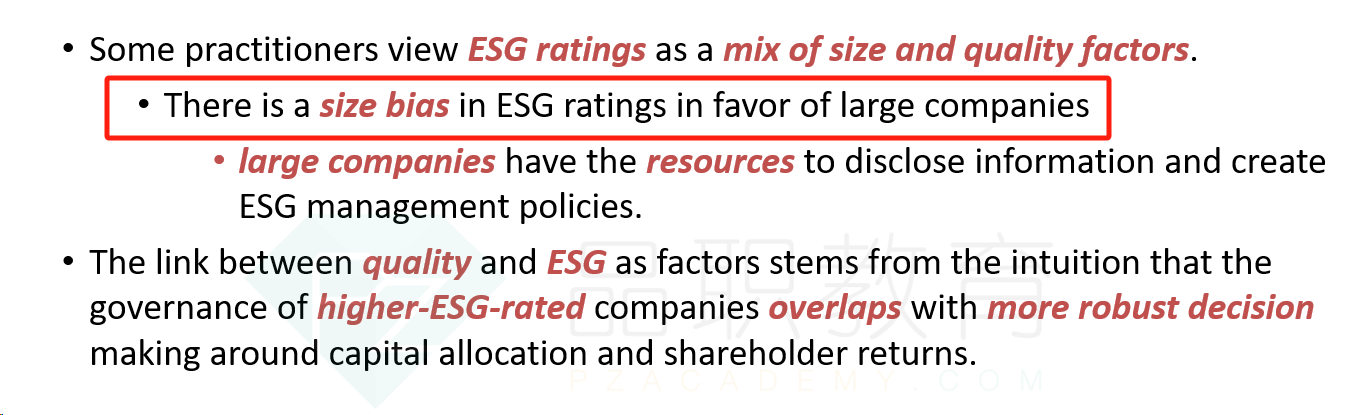

B. Correct because the ratings from many providers reveal a significant, underlying correlation with existing factors, such as value, quality, size, and momentum. In addition, there is a size bias in ESG ratings in favor of large companies because large companies have the resources to disclose information and create ESG management policies.

C. Incorrect because third-party data providers are developing increasingly sophisticated ESG ratings and scoring methodologies, but many fall short in describing ESG attributes as an uncorrelated, statistically independent factor. In fact, the ratings from many providers reveal a significant, underlying correlation with existing factors.

只提到公司的size factor有偏差,不是太单一了么