NO.PZ2023090501000080

问题如下:

A risk analyst at an asset management company is assessing the past performance of an internally managed equity fund. The analyst obtains the following information on the market and the fund over the last year:

•Treynor performance index for the fund: 8.00%

•Return of the market portfolio: 5.60%

•Beta of the fund: 0.65

•Risk-free rate of interest: 1.75%

Based on the information above, what is the Jensen's alpha for the equity fund over the same period?

选项:

A.

2.40%

B.

2.70%

C.

3.69%

D.

4.15%

解释:

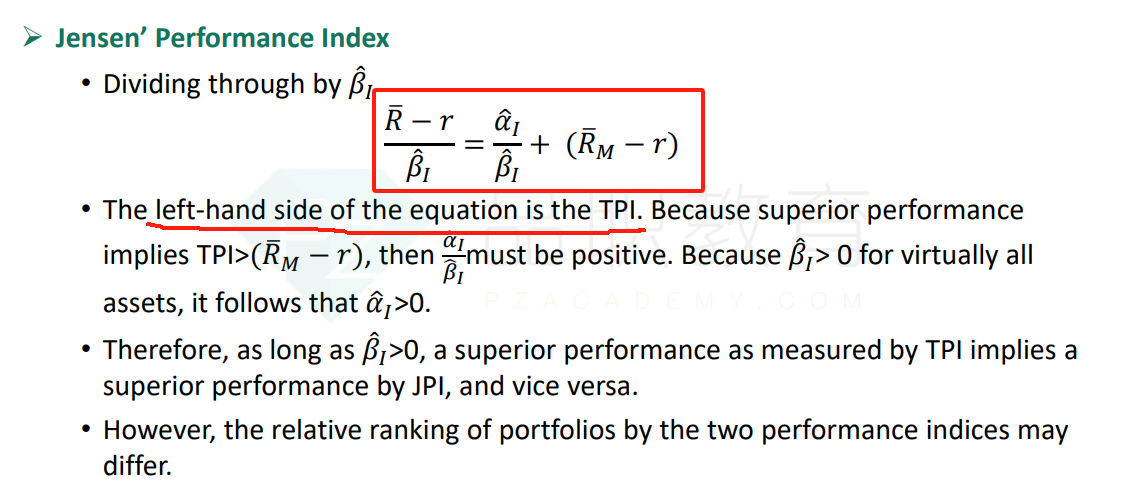

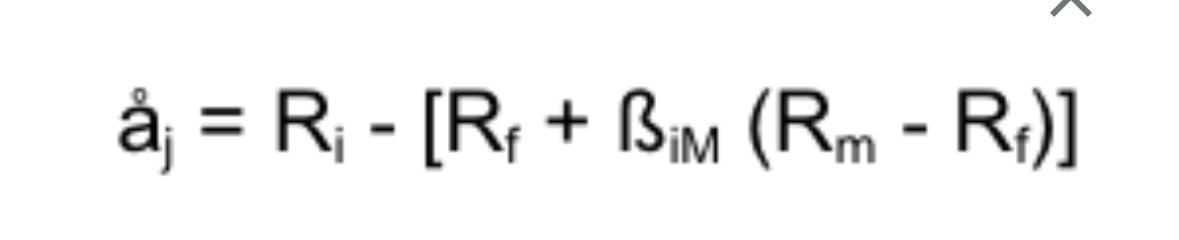

Explanation B is correct. The formula that shows the link between the Treynor performance index (TPI) and Jensen's alpha (a) is as follows:

TPI = α / beta + (Rm-Rf)

0.08= α /0.65 + (0.056-0.0175)

α = 0.026975

A is incorrect. This is obtained from 0.08-0.056=0.024.

C is incorrect. This is obtained from (0.08-0.056)/0.65=0.03692307692.

D is incorrect. This is obtained from 0.0175+0.024=0.0415.

Section Foundations of Risk Management

Learning

Objective Calculate, compare, and interpret the following performance measures: the Sharpe performance index, the Treynor performance index, the Jensen performance index, the tracking error, information ratio, and Sortino rati0.

Reference Global Association of Risk Professionals. Foundations of Risk Management. New York, NY: Pearson, 2022. Chapter 5. Modern Portfolio Theory and the Capital Asset Pricing Model.

可以列过程么?谢老師