NO.PZ201812170100000207

问题如下:

Based on Statement 2, the financial ratio most directly affected is the:

选项:

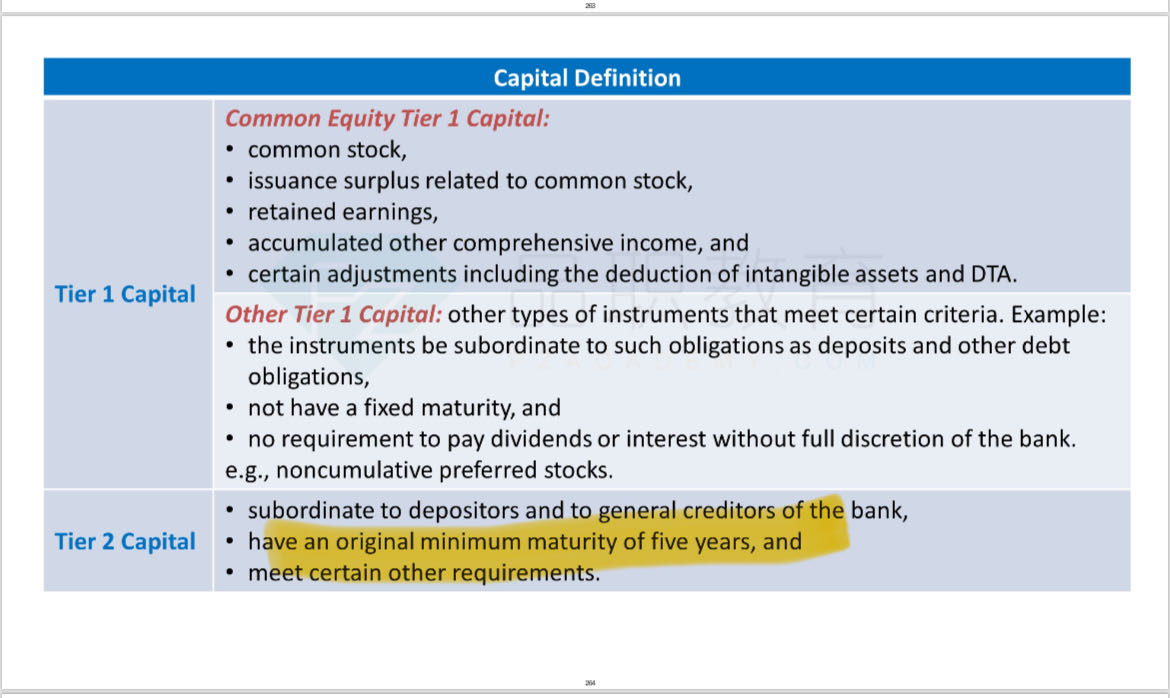

A.Tier 2 capital ratio.

net stable funding ratio.

liquidity coverage ratio.

解释:

C is correct.

Reverse repurchase agreements represent collateralized loans between a bank and a borrower. A reverse repo with a 30- day maturity is a highly liquid asset and thus would directly affect the liquidity coverage ratio (LCR). LCR evaluates short- term liquidity and represents the percentage of a bank’s expected cash outflows in relation to highly liquid assets.

解析:

考点:Analysis of Financial Institutions - Analyzing A Bank - The CAMELS Approach - Liquidity Position

Statement 2:在银行零售存款显著增长的时期,N-bank 在 30 天逆回购市场很活跃

逆回购是银行和借款人之间的抵押借款行为。比如 A 把债券先卖给 B,从 B 处获得资金,并约定一定时间后, A 再用钱把债券从 B 手里买回来

本质是一个融资的过程,这个债券其实就是抵押品。站在 A 的角度,属于 repurchase agreements。站在 B 的角度,就属于 reverse repurchase agreements

选项 A 错误。reverse repo 只是一种投资产品,不属于资本金,不会影响 Tier 2 capital ratio

选项 B 错误。净稳定融资比率,更关注「长期」流动性,从资产负债表的角度来理解,分子就是银行的资金来源,属于负债,分母是要求的稳定的资金来源。要求银行内部可用的稳定的资金来源是足以应对银行的「长期」业务的。

而 reverse repo 流动性很高(题干也说了是 30 天),因此不属于 stable funding,不影响净稳定融资比率,所以不选 B

选项 C 正确。题目说了现在是 30 天的逆回购,是短期,影响的应该是选项中,流动性最强的财务指标,即选项 C

reverse repo 只是一种投资产品,不属于资本金,不会影响 Tier 2 capital ratio

没有懂这句话的意思