NO.PZ2019042401000063

问题如下:

The risk committee of an equity mutual fund is reviewing a portfolio construction technique proposed by a new portfolio manager who has recently been allocated capital to manage. The fund typically grants its portfolio managers flexibility in selecting and implementing appropriate portfolio construction procedures but requires that any methodology adopted fulfill key risk control objectives set by the firm. Which of the following is correct regarding a portfolio construction technique and its approach to risk control?

选项:

A.The linear programming technique focuses on the pair-wise correlations of stocks rather than characterizing each stock along multiple dimensions of risk such as size, industry, volatility, or beta.

The screening technique ranks stocks by risk-adjusted alpha but it does not apply any additional risk control measures such as weighting the selected stocks by their relative capitalization

The stratification technique splits the list of stocks into categories and maintains risk control by overweighting the categories with lower risks and underweighting the categories with higher risks.

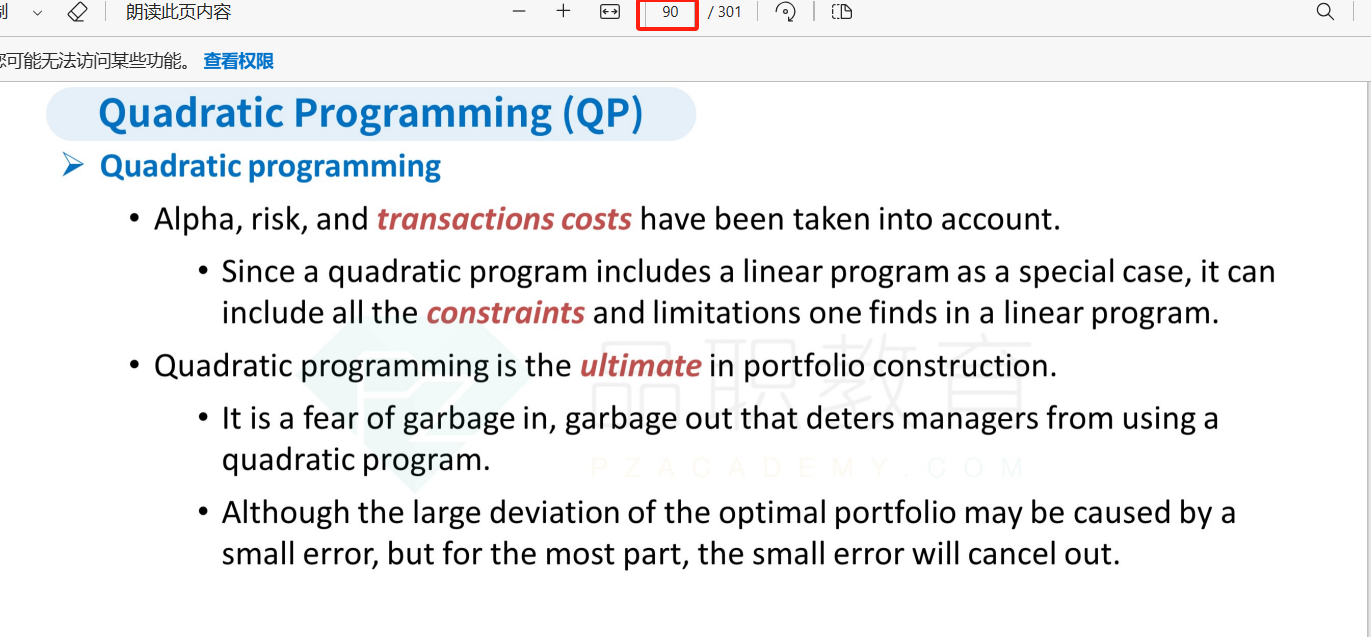

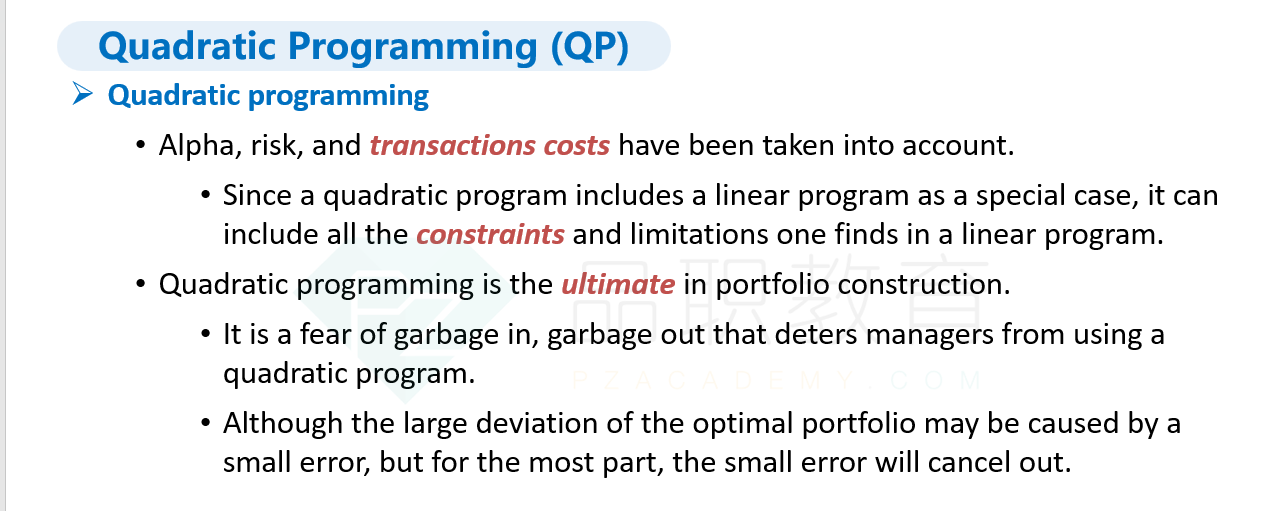

The quadratic programming technique takes into account additional risk parameters compared to other major portfolio construction techniques but also requires more inputs, which leads to more noise.

解释:

D is correct. Quadratic programming requires many more inputs than other portfolio construction techniques because it entails estimating not only alpha but also volatilities and pair-wise correlations between all assets in a portfolio as well as transaction costs. Quadratic programming is a powerful process but given the large number of inputs and the less than perfect nature of most data, it introduces the potential for noise and poor calibration.

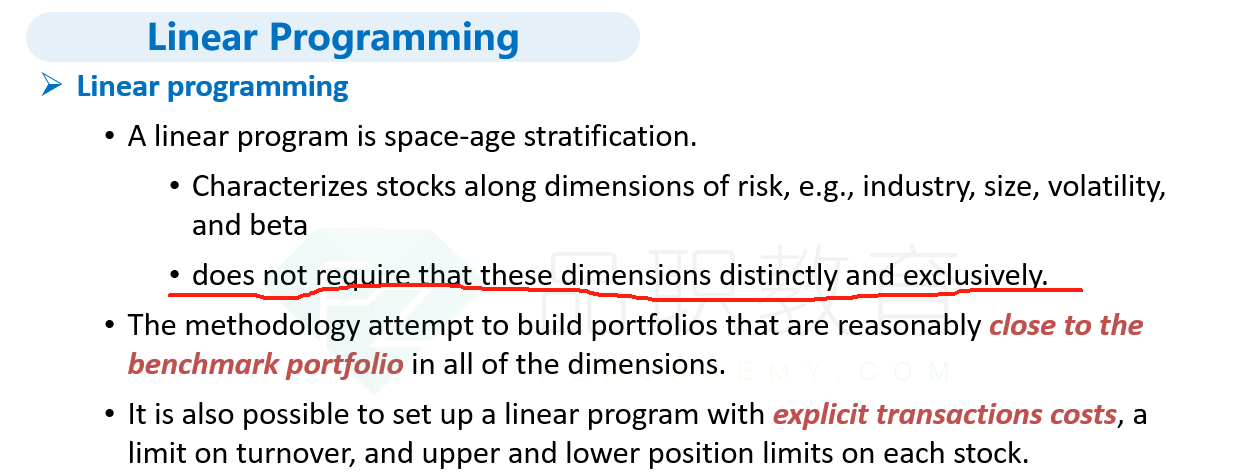

A is incorrect. The linear programming approach characterizes stocks along dimensions of risk, e.g., industry, size, volatility, and beta. The linear program does not require that these dimensions distinctly and exclusively partition the stocks. We can characterize stocks along all of these dimensions. The objective of the linear program is to maximize the portfolio’s alpha less transaction costs, while remaining close to the benchmark portfolio in the risk control dimensions

B is incorrect. Screening ranks stocks by alpha (not risk-adjusted alpha). It strives for risk control by choosing a sufficient number of stocks that meet the screening parameters and by weighting them (equal-weighting or capitalization-weighting) to avoid concentrations in any particular stock. However, screening does not necessarily select stocks evenly across sectors and can ignore entire sectors or classes of stocks if they do not pass the screen. Therefore, risk control in a screening process is fragmentary at best.

C is incorrect. It is true that stratification separates stocks into categories (for example, economic sectors). It implements risk control by ensuring that the weighting in each sector matches the benchmark weighting. However, it does not allow for overweighting one specific category over another.

如题