NO.PZ2019012201000024

问题如下:

Which of following is a feature regarding to the factor-tilting approach?

选项:

A.The approach specializes in taking stakes in listed companies and advocating changes for the purpose of producing a gain on the investment.

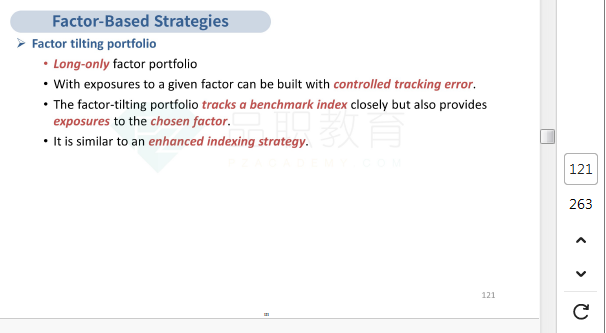

B.The approach tracks a benchmark index closely but also provides exposures to the chosen factor.

C.A long/short portfolio is typically formed by going long the best quantile and shorting the worst quantile.

解释:

B is correct.

考点:Top-Down and Other Strategies

解析: 因子倾斜策略在密切跟踪基准指数的同时对看好的因子主动承担一定风险。

之前做的笔记,忘记在哪看到的了,这三个是对的吗?尤其是,factor-tilting可以理解为semi-active?

A: advocating changes for the purpose of producing a gain on the investment->activist strategies

B: semi-active->factor tilting approach

C: long/short->hedged portfolio approach