NO.PZ2023052301000094

问题如下:

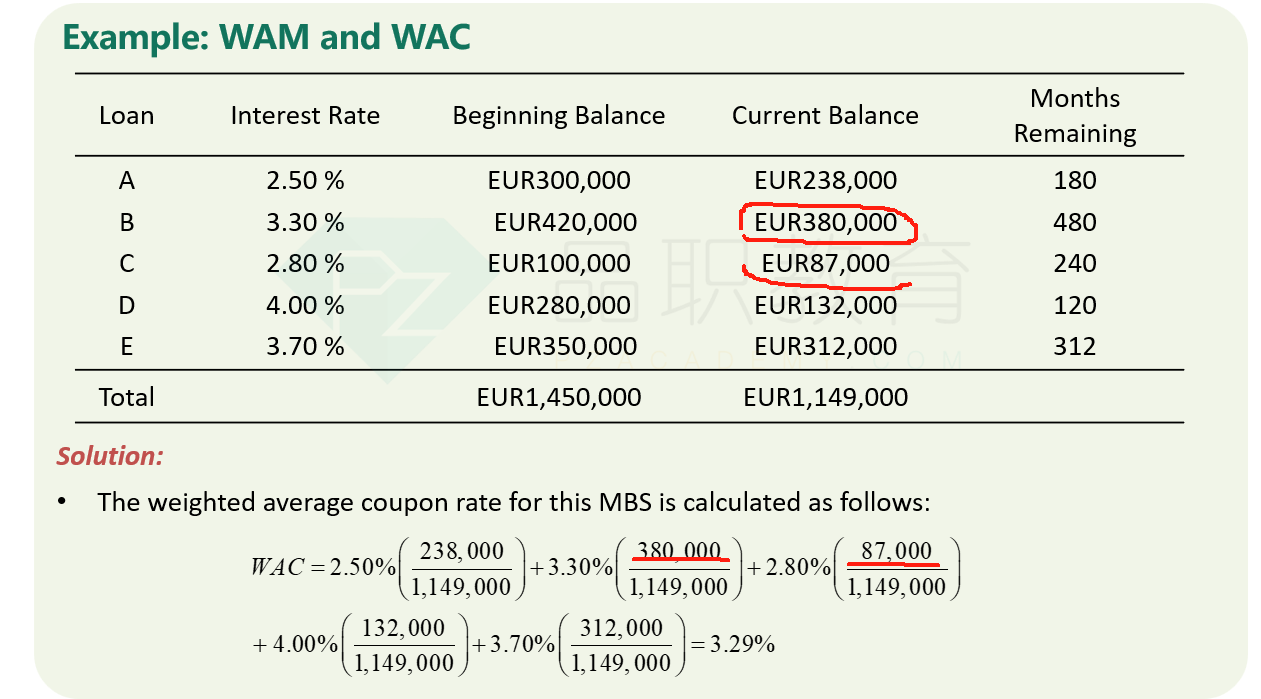

Shown below are five mortgages that comprise the entire pool in a mortgage-backed security.

The WAM for this security is closest to:

选项:

A.208 months

B.224 months

C.236 months

解释:

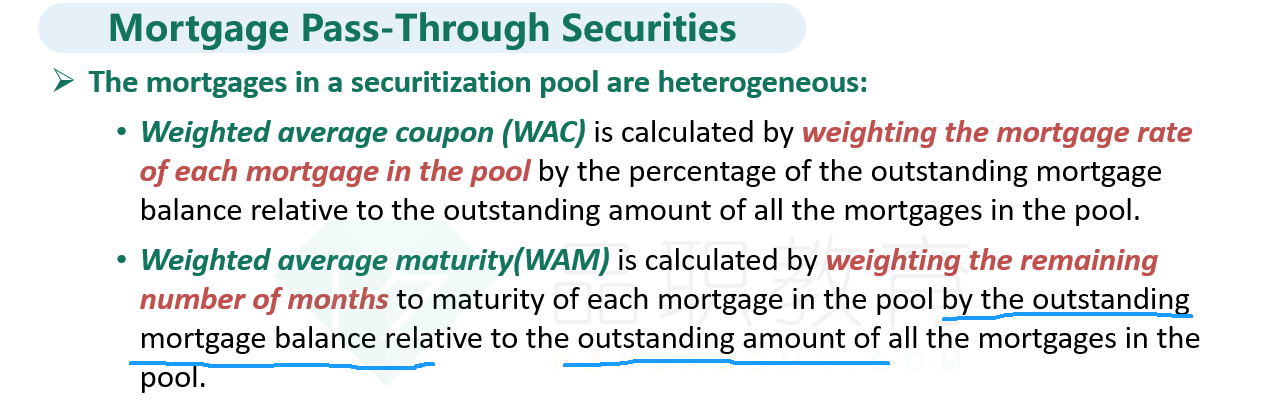

The correct answer is C. The weighted average maturity is calculated by weighting the number of months to maturity for each mortgage in the pool by the percentage of the outstanding mortgage balance relative to the outstanding amount of all the mortgages in the pool, as shown in the following equation:

如题