NO.PZ2022071105000020

问题如下:

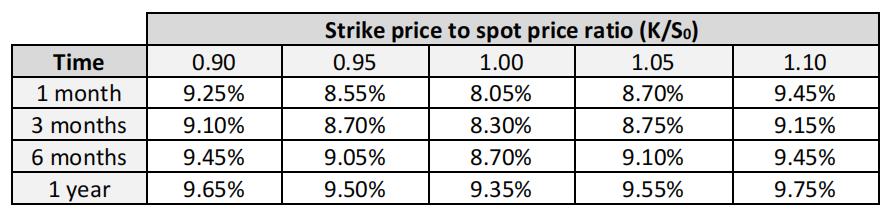

A market-maker on the foreign exchange desk at an investment bank has been asked to quote a call option that

expires in 7 months and has a strike price (K) to spot price (S0) ratio of 1.075. The market-maker references the

following implied volatility surface when providing the quote:

What implied volatility should the market-maker use to provide the quote?

选项:

A.9.18%

B.9.28%

C.9.34%

D.9.65%

解释:

中文解析:

C是正确的。为了找到正确的隐含波动率,我们需要在6个月的K/S0 = 1.05的期权和1年期的K/S0=1.10的期权之间进行两次插值。

首先:

9.10 + 1/6*(9.55-9.10) = 9.175……对应1年期1.05的期权;

9.45 + 1/6*(9.75-9.45) = 9.5……对应1年期1.10的期权。

因为1.075是1.05和1.1的平均数,所以我们把上面两个数字求平均值,(9.175+9.5)/2 = 9.3375

C is correct. There are two interpolations to be made to find the correct reference implied

volatility. One is related to time and the other is the related to the K/S0 ratio.

To find the 7-month reference implied volatility with a K/S0 ratio of 1.075, we need to

interpolate between 6-month and 1-year at the K/S0 ratios of 1.05 and 1.10. And to do

this, we add one month’s worth of the difference between the 6-month and 1-year

volatilities to the 6-month volatility:

9.10 + 1/6*(9.55-9.10) = 9.175

9.45 + 1/6*(9.75-9.45) = 9.5

We then take the simple average of these two numbers since 1.075 is exactly between

1.05 and 1.1:

(9.175+9.5)/2 = 9.3375

A is incorrect. This uses the volatilities at the 1.05 K/S0 ratio and only interpolates time.

B is incorrect. This uses the volatilities at 6 months and only interpolates the K/S0 ratio.

D is incorrect. This uses the volatilities at 1 year and only interpolates the K/S0 ratio.

如题