NO.PZ2023090401000093

问题如下:

Question Two risk analysts are attending a seminar on the topic of modern portfolio theory. One of the presentations in the seminar focuses on the efficient frontier, the capital market line, and the CAPM. Assuming the CAPM holds, which of the following observations is correct for the analysts to make?

选项:

A.

The capital market line always has a positive slope and its steepness depends on the market risk premium and the volatility of the market portfolio.

B.

The capital market line is the straight line connecting the risk-free asset with the zero-beta minimum-variance portfolio.

C.

The portfolio of risky assets with the lowest standard deviation on the efficient frontier is typically held by the least risk averse investors.

D.

The efficient frontier indicates that different individuals hold different portfolios of risky assets based upon their individual forecasts for asset returns.

解释:

Explanation:

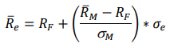

A is correct. The capital market line connects the risk-free asset with the market portfolio, which is the efficient portfolio at which the capital market line is tangent to the efficient frontier. The equation of the capital market line is as follows:

where the subscript e denotes an efficient portfolio. Since the shape of the efficient frontier is dictated by the market risk premium, RM-RF, and the volatility of the market, the slope of the capital market line will also be dependent on these two factors.

B is incorrect. As said in A above, the capital market line connects the risk-free asset with the market portfolio (which by definition has a beta of 1).

C is incorrect. The implication of the CML is that all investors should allocate to two investments: the risk-free asset and the market portfolio. Investors with little tolerance for risk will allocate most of their funds to the risk-free asset.

D is incorrect. One of the crucial assumptions for the derivation of CAPM is that all market participants have the same expectations, and therefore have the same forecast for asset returns. Additionally, as mentioned above, all investors hold the same portfolio of risky assets, which is the market portfolio.

Section: Foundations of Risk Management

Learning Objective: Understand the derivation and components of the CAPM. Interpret and compare the capital market line and the security market line.

Reference: Global Association of Risk Professionals. Foundations of Risk Management. New York, NY: Pearson, 2022. Chapter 5. Modern Portfolio Theory and the Capital Asset Pricing Model.

这道题怎么理解,解释一下