NO.PZ2023090401000096

问题如下:

Question A risk analyst at a growing bank is concerned about a loan exposure to a large manufacturing company which is losing significant market share in its industry. The analyst considers the use of different credit risk transfer mechanisms, including CDS, to manage this exposure. Which of the following statements correctly describes an appropriate benefit of using CDS in this situation?

选项:

A.

CDS quantify the manufacturing company’s default risk and allow the bank to monitor changes in this risk on a real-time basis.

B.

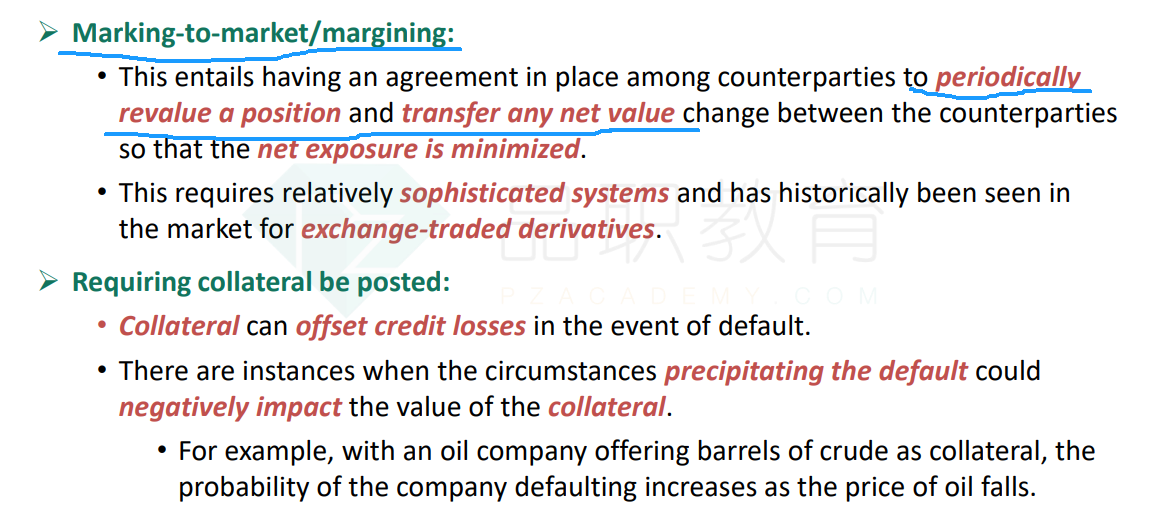

CDS provide an agreement to periodically revalue the loan and transfer any net value change.

C.

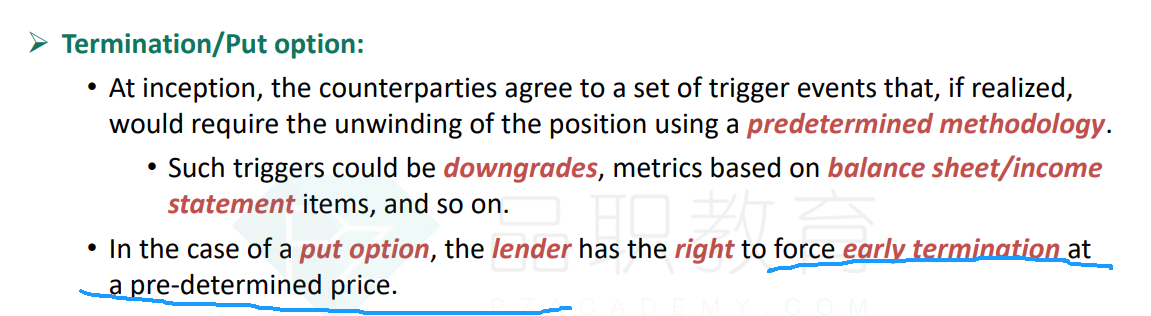

CDS require the manufacturing company to pay back the loan in full at an earlier point in time.

D.

CDS allow the bank to offset its exposure to the company with loan exposures to other manufacturing companies.

解释:

Explanation A is correct. CDS (or credit default swaps) are credit derivatives that quantify a company’s default risk and allow the bank to monitor changes in the company’s default risk on a real-time basis. This is an improvement over credit ratings, which only update assessments of companies’ default risk on a periodic basis. B is incorrect. This would be a feature of marking-to-market/margining. C is incorrect. This would be an example of a termination/put option mechanism. D is incorrect. CDS do not provide an offset using loan exposures to other counterparties. A separate transfer mechanism, netting, can be used to offset negative and positive exposures to the same counterparty but this statement does not correctly describe netting either.

Section Foundations of Risk Management Learning Objective Compare different types of credit derivatives, explain their applications, and describe their advantages.

Reference Global Association of Risk Professionals. Foundations of Risk Management. New York, NY: Pearson, 2022. Chapter 4. Credit Risk Transfer Mechanisms.

这道题选项是什么意思啊,怎么选择呢