NO.PZ2019042401000072

问题如下:

An investor is performing due diligence on a hedge fund that invests in illiquid assets. The investor obtains monthly return data on the fund but is concerned about possible bias in the data, which may provide a misleading impression of the fund’s risk profile. Which of the following would be a correct assessment for the investor to make?

选项:

A.

Volatility will be artificially high, giving the appearance of high total risk, which can be corrected by taking into account the resulting positive autocorrelation of returns.

B.

Correlations with other asset classes will be artificially high, giving the appearance of high systematic risk, which can be corrected using enlarged regressions with additional lags of the market factors and summing the coefficients across lags.

C.

Correlations with other asset classes will be artificially low, giving the appearance of low systematic risk, which can be corrected using enlarged regressions with additional lags of the market factors and summing the coefficients across lags.

D.

Volatility will be artificially low, giving the appearance of low total risk, which can be corrected by taking into account the resulting negative autocorrelation of returns.

解释:

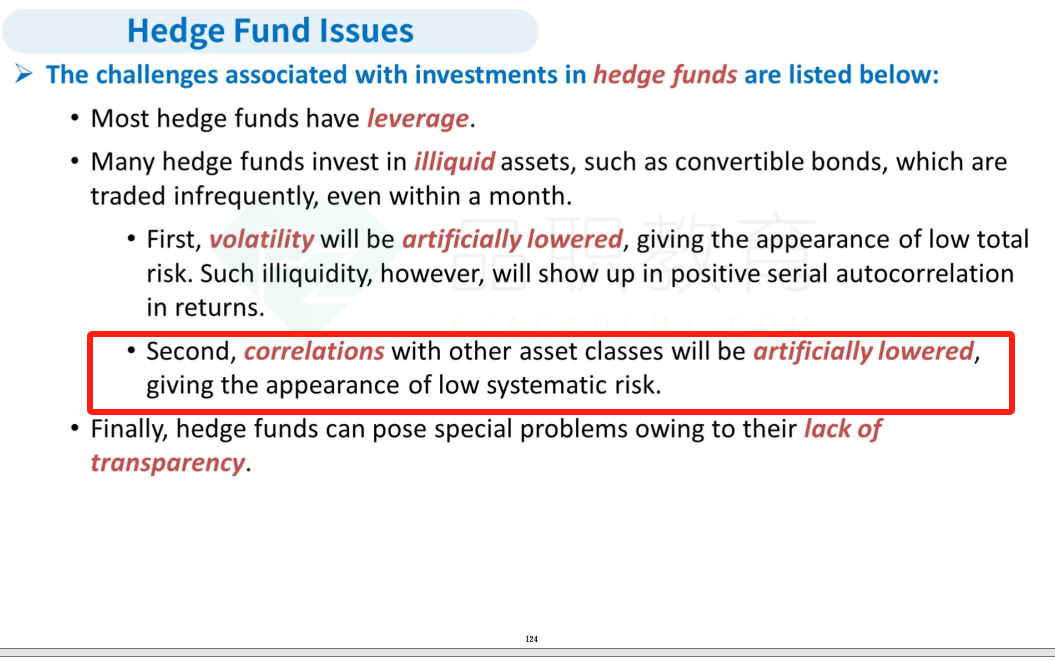

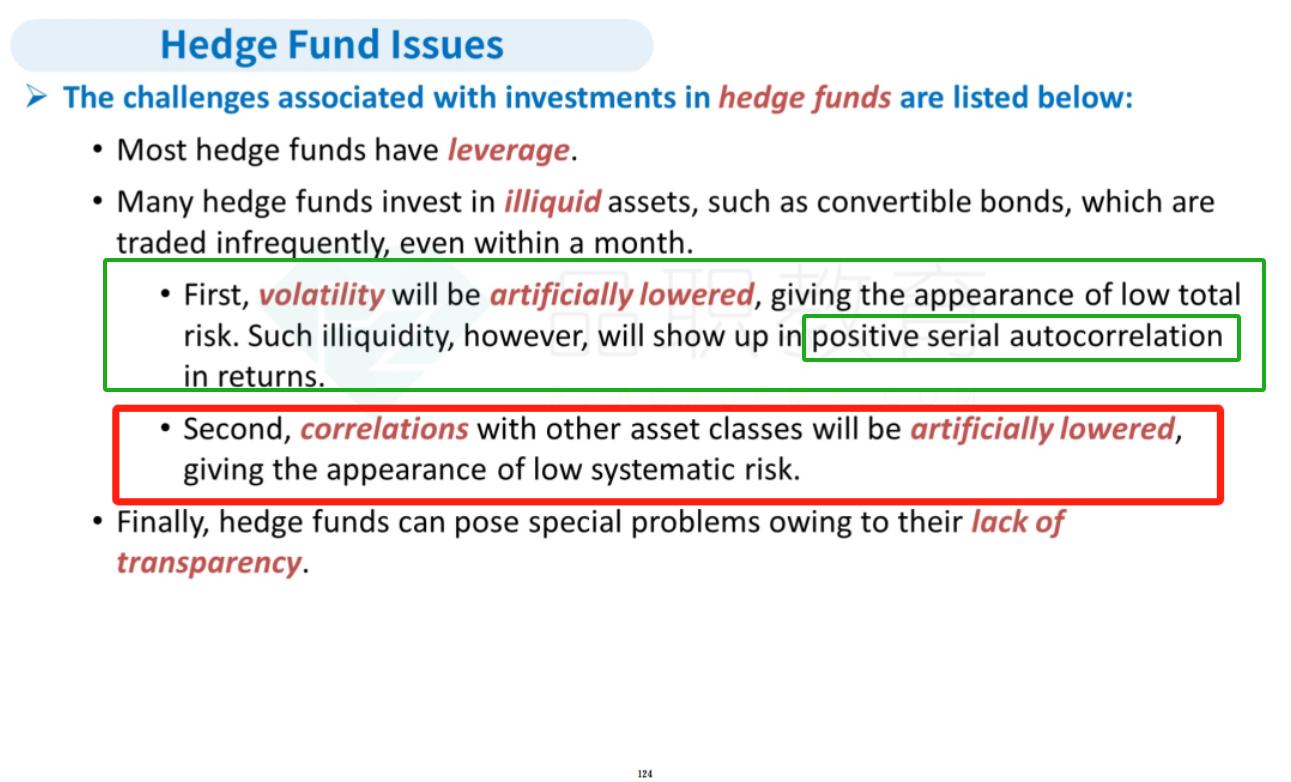

C is correct. Illiquid assets, such as convertible bonds, are traded infrequently. Risk measures based on monthly returns give a misleading picture of risk because the closing net asset value (NAV) does not reflect recent transaction prices. This creates two types of biases: First, correlations with other asset classes will be artificially lowered, giving the appearance of low systematic risk. This can be corrected using enlarged regressions with additional lags of the market factors and summing the coefficients across lags. Second, volatility will be artificially lowered, giving the appearance of low total risk. Such illiquidity, however, will show up in positive serial autocorrelation in returns. Biases in volatility measures can be corrected by taking this autocorrelation into account when extrapolating risk to longer horizons.

A is incorrect. Volatility will be artificially lowered, making it appear that total risk is low.

B is incorrect. Correlations with other asset classes will be artificially lowered.

D is incorrect. The illiquidity will exhibit itself through positive serial autocorrelation in returns.

没有找到这个考点出自哪个章节?