NO.PZ2019042401000060

问题如下:

A portfolio manager at a pension fund is presenting on investment strategies during a training for newly-hired portfolio analysts. The manager discusses low volatility strategies, illustrates historical performance measures of firms that apply these strategies, and draws attention to the benchmarks used. Which of the following statements about low volatility strategies would be correct for the manager to make during the presentation?

选项:

A.

The strategies tend to generate low alphas if the benchmark used is adjusted for risk and high alphas otherwise.

B.

The strategies tend to have negative alphas relative to dynamic factors such as value or momentum.

C.

The strategies tend to generate high alphas over the risk-free rate but negligible alphas over any other benchmark.

D.

The strategies tend to have significant alphas relative to standard market capitalization benchmarks.

解释:

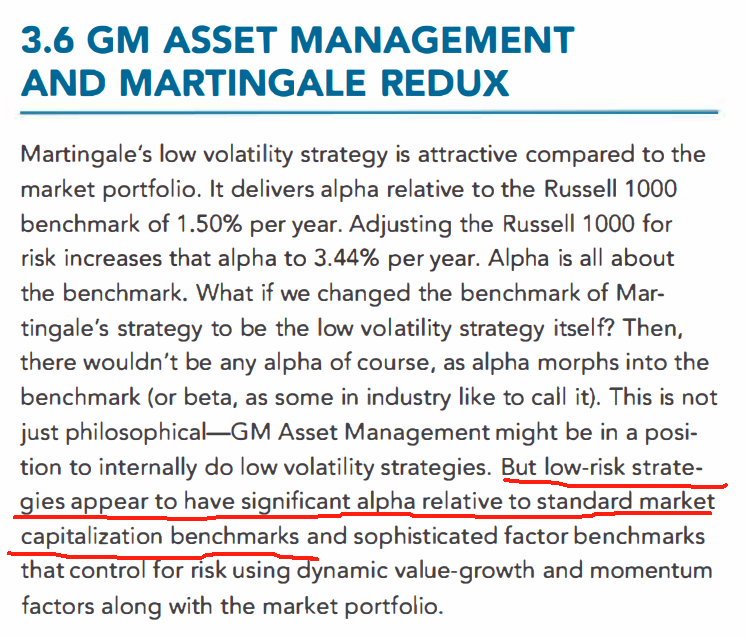

D is correct. Low-risk strategies appear to have significant alpha relative to standard market capitalization benchmarks and sophisticated factor benchmarks that control for risk using dynamic value and momentum factors.

A is incorrect. We can’t say that. Alpha is very much dependent on the benchmark used as well as whether or not that benchmark is adjusted for risk.

B is incorrect. See explanation for D. C is incorrect. See explanation for D.

请问考的哪个知识点,没理解这道题考的什么?