NO.PZ2015121801000091

问题如下:

With respect to return-generating models, which of the following statements is most accurate? Return-generating models are used to directly estimate the:

选项:

A.

expected return of a security.

B.

weights of securities in a portfolio.

C.

parameters of the capital market line.

解释:

A is correct.

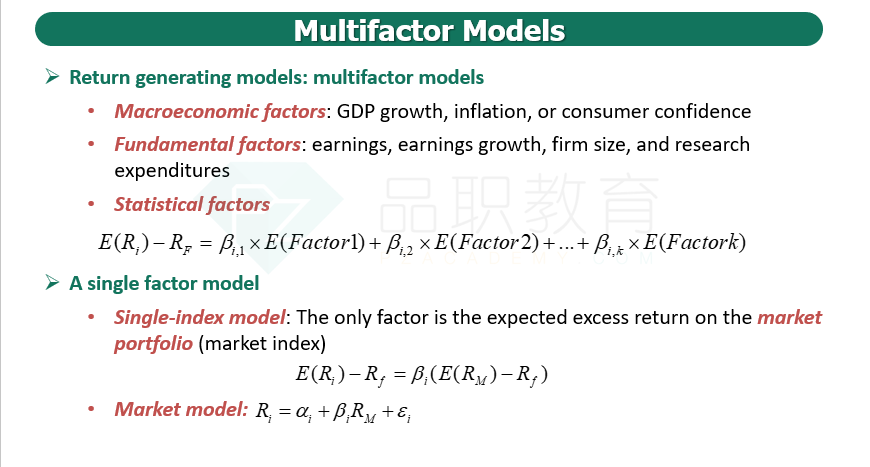

In the market model, Ri =αi +βiRm +ei, the intercept, αi, and slope coefficient,βi, are estimated using historical security and market returns. These parameter estimates then are used to predict firm-specific returns that a security may earn in a future period.

不是说CAMP是看预期收益率的;这个Ri=α+β*Rm+残差项是通过真实历史数据,回归出α和β吗?这道题问算预期收益率的,怎么又用这个了呢?