NO.PZ202208160100000104

问题如下:

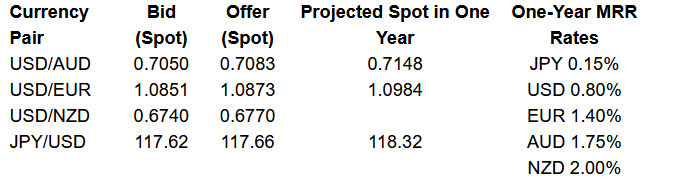

Based on the data in Exhibit 1, the bid EUR/AUD cross-rate implied by the interbank market is closest to:选项:

A.0.6497.B.0.6484. C.0.7650.

解释:

Solution

B is correct. The bid EUR/AUD is calculated as follows:

Sell EUR/Buy AUD = Sell EUR/Buy USD × Sell USD/Buy AUD, which will require the inversion of USD/EUR to EUR/USD.

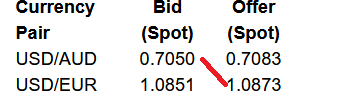

Given the USD/EUR quotes of 1.0851/1.0873, take the inverse of each and interchange the bid and offer, such that the USD/EUR quotes are (1/1.0873)/(1/1.0851) = 0.91971/0.92157 = 0.9197/0.9216.

Then multiply the EUR/USD and USD/AUD bid quotes:

Bid: 0.9197 × 0.7050 = 0.64839 = 0.6484

Thus, the USD/EUR bid cross-rate implied by the interbank market is 0.6484.

A is incorrect. The candidate inverts the USD/EUR quotes but does not interchange the bid and offer and thus incorrectly calculates the interbank market bid cross-rate using the offer cross-rate.

Bid: 0.9216 × 0.7050 = 0.64973 = 0.6497

Thus, the EUR/AUD bid cross-rate implied by the interbank market is 0.6497.

C is incorrect. The candidate incorrectly multiplies the two bid rates to calculate the interbank market cross-rate.

Bid: 0.7050 × 1.0851 = 0.76500 = 0.7650

Thus, the EUR/AUD bid cross-rate implied by the interbank market is 0.7650.

中文解析:

B是正确的。投标欧元/澳元的计算方法如下:

卖出欧元/买入澳元=卖出欧元/买入美元×卖出美元/买入澳元,这需要将美元/欧元反转为欧元/美元。

假设美元/欧元的报价为1.0851/1.0873,取两者的倒数并交换买入价和卖出价,这样美元/欧元的报价为(1/1.0873)/(1/1.0851)= 0.91971/0.92157 = 0.9197/0.9216。

然后将欧元/美元和美元/澳元的竞价报价相乘:

竞价:0.9197 × 0.7050 = 0.64839 = 0.6484

因此,银行间市场隐含的美元/欧元买入价交叉利率为0.6484。

A是不正确的。候选人将美元/欧元的报价颠倒,但没有交换买入价和卖出价,因此使用卖出价交叉利率错误地计算了银行间市场的买入价交叉利率。

竞价:0.9216 × 0.7050 = 0.64973 = 0.6497

因此,银行间市场隐含的欧元/澳元买入价交叉利率为0.6497。

C是不正确的。候选人错误地将两个投标利率相乘以计算银行间市场交叉利率。

竞价:0.7050 × 1.0851 = 0.76500 = 0.7650

因此,银行间市场隐含的欧元/澳元买入价交叉利率为0.7650。

为什么先求倒数再乘,不能先除再求倒数呢?