Inflection Capital Case Scenario

Derek Mulaney is the head trader at Inflection Capital, a Boston-based investment

management firm offering traditional and alternative investment strategies. Mulaney

leads a three-person trading team consisting of himself, Feng Shui, and Abagail

Morrison. The trading team works closely with Inflection’s portfolio managers, analysts,

and compliance team in the execution of the firm’s investment strategies.

As part of his morning team meeting, Mulaney often reviews trading situations with Shui

and Morrison. He brings up an example that recently occurred while trading for

Inflection’s hedge fund. The portfolio manager, Chris Largent, was listening to a 10:00

a.m. earnings call for NeuvoGen (NGEN), a midsize biotech company, during which

management announced additional unfavorable news. Largent determined the market

had significantly underreacted to the news and wanted to set up a trade to exploit this

potential alpha opportunity. Largent communicated a sell order to Mulaney to establish a

short position for the fund representing approximately 3% of expected trading volume

for the stock that day. Mulaney describes how he used a trading algorithm to sell the

shares, adding that some algorithms are more suitable to use than others, depending

on the situation.

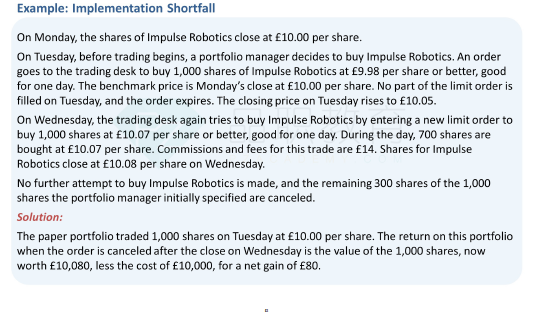

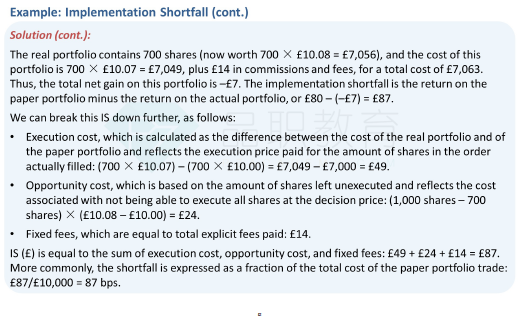

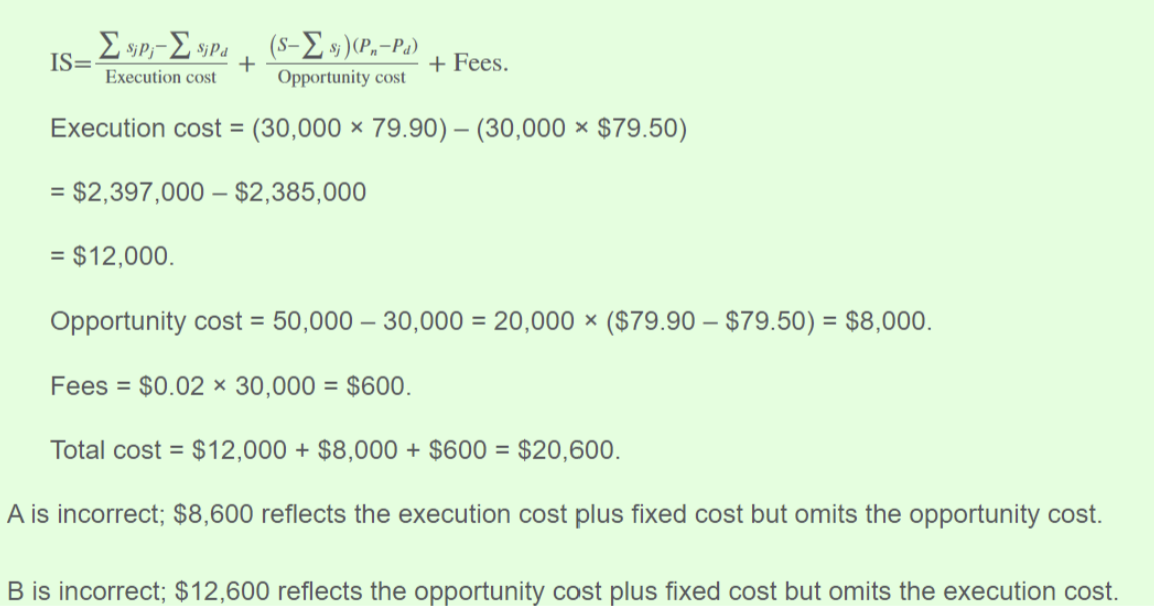

Morrison has been working on executing a sell order to liquidate shares in Acme

Industrials (ACME). The closing price on Tuesday was $79.90. Morrison received the

order from Wright before the market open on Wednesday morning to sell 50,000 ACME

shares with a day limit of $80.00. No part of the order is filled on Wednesday, and the

stock closes the day at $79.60. On Thursday morning, Morrison instructed a new day

order to sell the 50,000 shares at $79.50; 30,000 shares were sold at $79.50 per share,

with resulting commissions and fees for the trade of $0.02 per share. Shares for ACME

closed the day Thursday at a price of $79.40 per share. No further attempts were made

to sell the unfilled 20,000 shares, which were canceled.

Shui is instructed to execute a buy order of TeXelence (TEXX), a small-cap technology

stock. Shui is able to execute the order over the course of 30 minutes and received an

average price of $50.55. The price at the time the order was placed is $50.45. The

volume-weighted average price (VWAP) over the trading horizon was $50.52, and the

time-weighted average price (TWAP) over the horizon was $50.57, with a closing price

later that day of $50.60. The market rose during the trading horizon, with an index

arrival price of 1,010 and a VWAP of 1,015. Shui calculates that TEXX has a beta to the

index of 1.30.

At the end of each trading week, Mulaney holds a strategy meeting with Shui and

Morrison to evaluate trade execution and to discuss strategies for improvement in the

future. They are discussing trade implementation in different markets as they begin to

support a new macro-hedge fund that frequently trades in emerging market equities and

often uses derivatives to implement its strategy.

Morrison is discussing trading trends and makes the following observation: “In recent

years, average trade sizes appear to be increasing, and in emerging markets, a similar

volume of equity trading is now taking place on dark pools as on ‘lit’ exchanges.”

Shui comments, “For exchange-traded derivatives, market transparency is similar to

that of exchange-traded equities, with trade price, size, quote, and depth of book all

publicly available. I believe we should explore algorithmic trading in futures markets,

where it is more evolved than it is for options markets.”

Mulaney adds, “We can also explore the use of over-the-counter (OTC) derivatives.

Liquidity has increased for OTC instruments, even for those not suited to central

clearing, and average trade size is still relatively small, which could align well with the

needs of the fund.”

The implementation shortfall for the ACME trade is closest to:

1. $8,600.

1. $12,600.

1. $20,600.

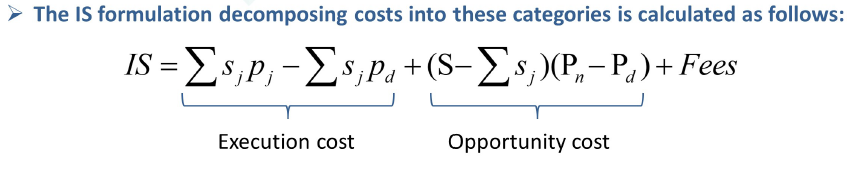

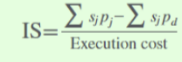

Solution

C is correct. The implementation shortfall (IS) is the combination of execution cost,

opportunity cost, and fees. Mathematically, IS is calculated as follows:

IS = Paper return – Actual return

The paper return shows the hypothetical return that the fund would have received if the

manager were able to transact all shares at the desired decision price and without any

associated costs or fees (i.e., with no friction)

should Pn=$79.40? I don't understand the calculations in the answer. I understnad Pd is $79.90, and Pj is $79.50. Could you show the two methods to calculate the shortfall cost? Thank you!!