NO.PZ2023090506000003

问题如下:

The annual report of company XYZ contains the following disclosures:

- Disclosure 1: “XYZ’s management compensation is based on exceeding a target EPS growth rate.”

- Disclosure 2: “XYZ’s management does not change the required rate of return when evaluating capital projects based on whether they are financed by internal or external sources.”

- Disclosure 3: “When evaluating investment projects, XYZ prepares cashflow projections based on inflation-adjusted cash flows and discounts them using real rates.”

选项:

A.

Disclosure 1

B.

Disclosure 2

C.

Disclosure 3

解释:

A is correct. Positive-NPV investment projects can reduce, rather than increase, EPS in the near term, even though they increase shareholder value. Management compensation should incorporate a longer-term perspective and a measure that better considers required rates of return, such as ROIC.

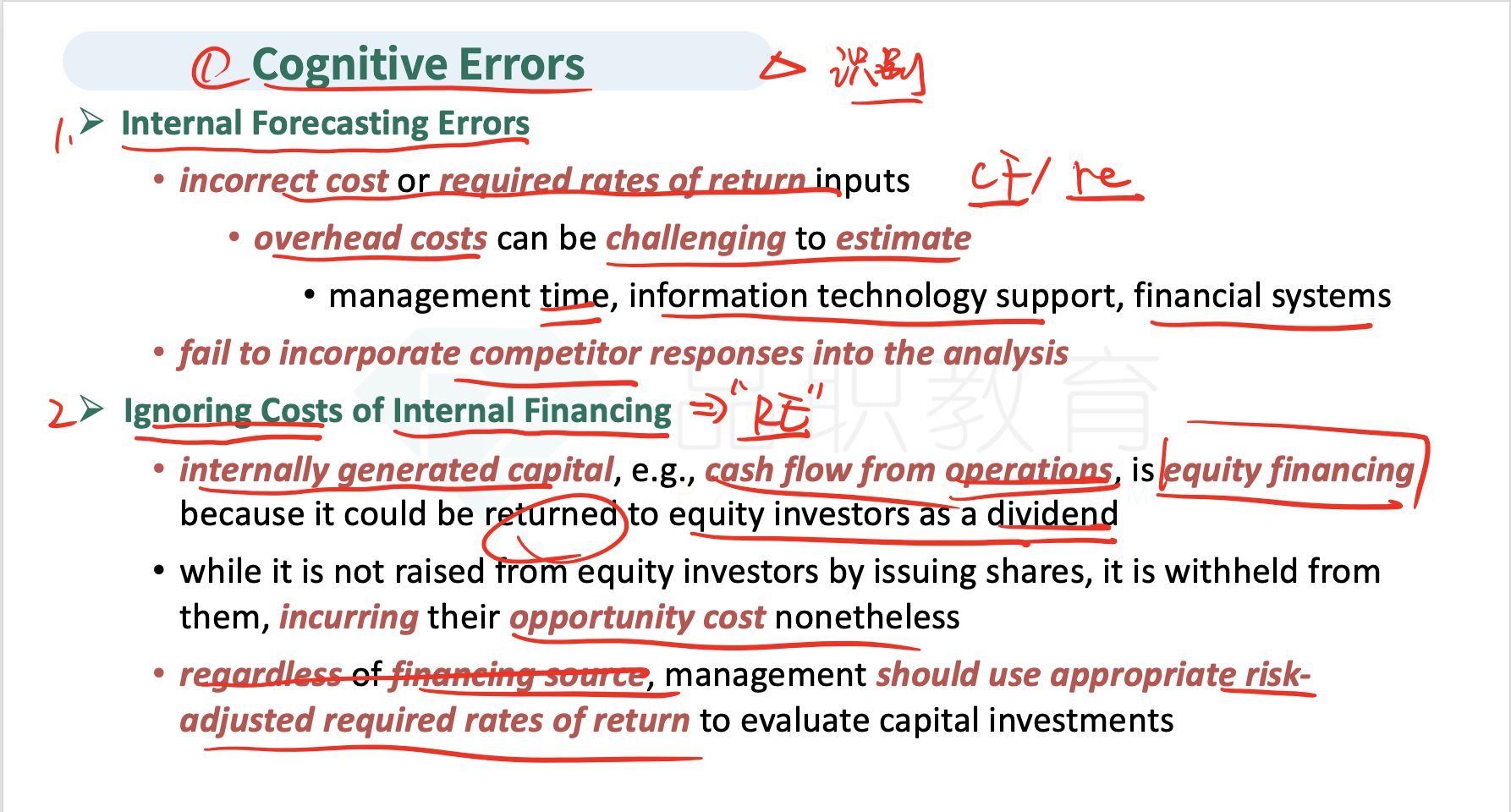

B is incorrect because internally generated capital, such as cash flow from operations, is equity financing and it could be returned to equity investors as a dividend. Regardless of the financing source, management should use appropriate risk-adjusted required rates of return to evaluate capital investments.

C is incorrect because companies may perform analysis in either nominal or real terms, but the approach to cash flows and the discount rate should be consistent. That is, nominal cash flows should be discounted at a nominal discount rate, and real (inflation-adjusted) cash flows should be discounted at a real rate.

课件里说到应考虑internal financing,所以应该用risk adjusted rate of return,感觉2 说的意思是不要调整 请老师