02:16 (2X)

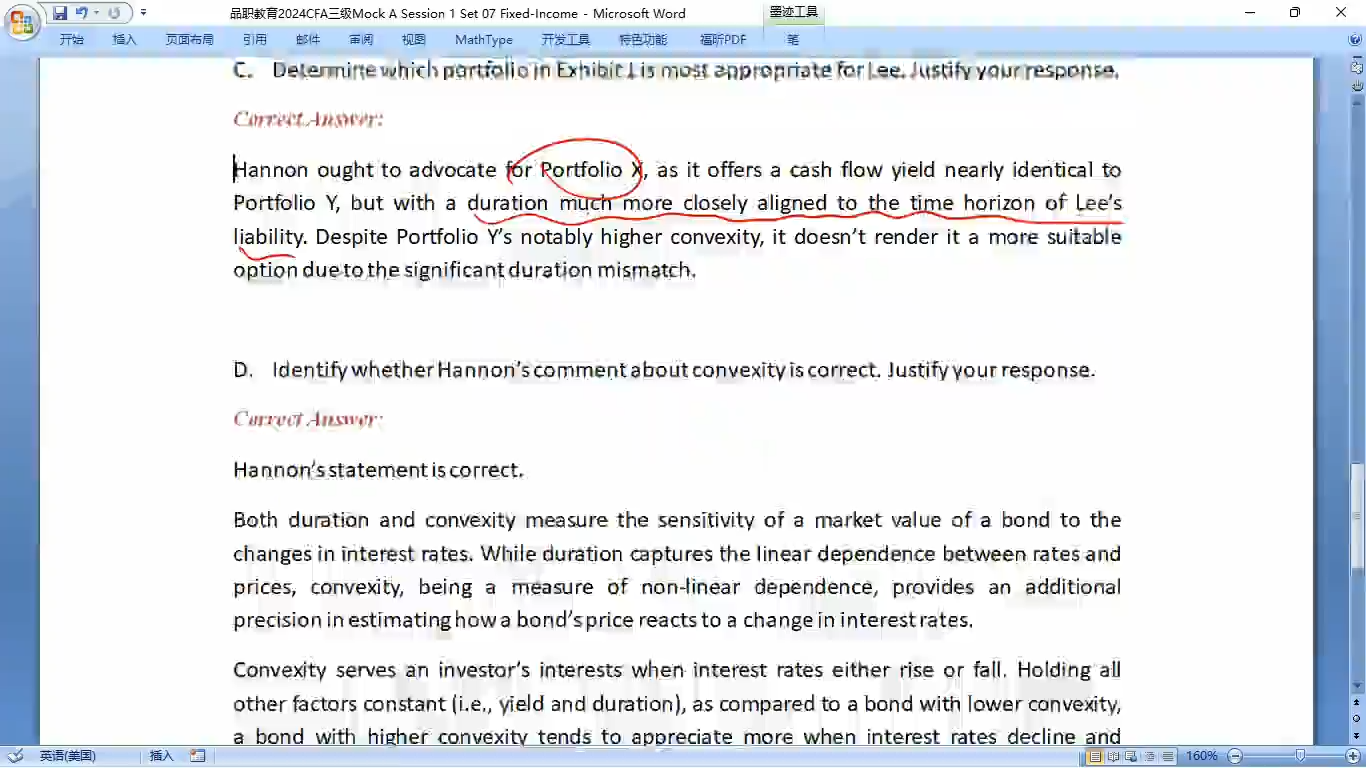

请问这里的答案里的第二句解释是不是写错了?"Despite Portfolio Y's notable higher convexity, it doesnt render it a more suitable option..." 这个despite用的听起来像是higher convexity更好一样。但是immunization不是应该convexity越低越好吗?

发亮_品职助教 · 2024年02月13日

是的,仅看答案的话有这个意味在,但这个答案是针对题干的问题作出的回复,联系上下文没有矛盾哈。

因为对应的题干是这句:

Hannon explains that assuming constant yield and duration, higher convexity is a beneficial property of a fixed-income portfolio.

题干的这句描述就是在说Convexity对于FI portfolio来讲是一个beneficial的属性、优质属性。其实就是在说Convexity越高越好,那按照这个说法看起来应该是Portfolio Y更合适。

紧接着回答的时候,答案作出了反驳:

尽管组合Y的Convexity更大(Convexity的确是债券的优质属性,但是我们现在做的是Duration-matching,Duration-matching并不追求Convexity最大,Duration-matching追求的是资产与负债的数据匹配),所以导致Portfolio Y并不是最佳的组合。

所以答案的Despite....是针对题干上面标黄这句的反驳

Despite Portfolio Y’s notably higher convexity, it doesn’t render it a more suitable option due to the significant duration mismatch

要避免歧义的话,可以这么回复:

although convexity is a beneficial property for fixed-income active investment, a single liability duration matching strategy should have convexity as small as possible to minimize structural risk