18:57 (2X)

最后一句是判断bullet/barbell变成ladder后RI risk和convexity的变化,题目中是怎么看出来是“变成ladder”的?是我题干看漏了,还是题目没说清楚?

pzqa31 · 2024年02月06日

嗨,从没放弃的小努力你好:

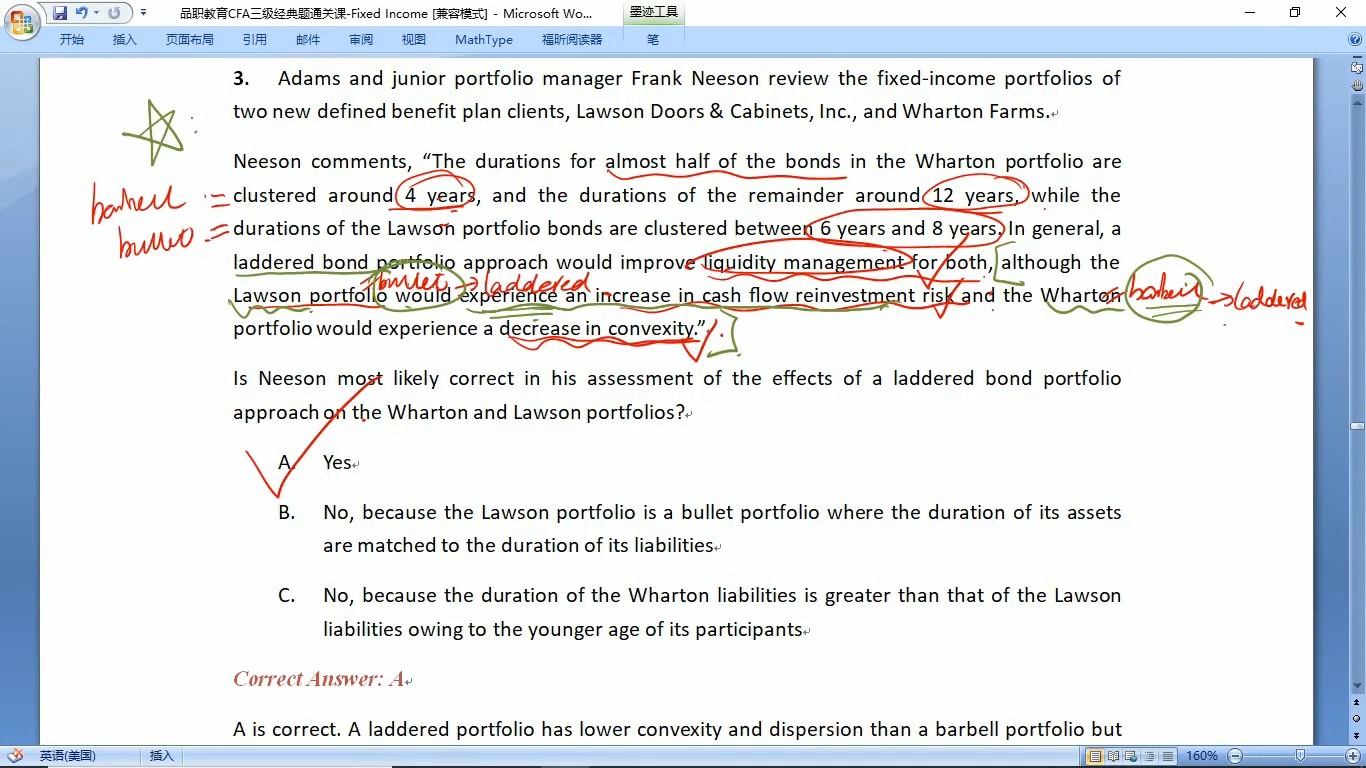

“The durations for almost half of the bonds in the Wharton portfolio are clustered around 4 years, and the durations of the remainder around 12 years,

---

W同学的portfolio是一个barbell。

while the durations of the Lawson portfolio bonds are clustered between 6 years and 8 years.

----

L同学的portfolio是一个bullet。

In general, a laddered bond portfolio approach would improve liquidity management for both,

---

这句话意思是将两个portfolio改造成laddered portoflio会提高他们的流动性。

although the Lawson portfolio would experience an increase in cash flow reinvestment risk and the Wharton portfolio would experience a decrease in convexity.”

---

尽管bullet portfolio的reinvestment risk会上升,barbell portfolio的convexity会下降。

这段话的表述都是正确的。

对应的知识点:

Laddered portfolio的现金流是最分散,如果比较convexity,除了现金流分散情况以外,还要限制duration与barbell、bullet相等,那么laddered 的convexity就不是最大的了。

----------------------------------------------加油吧,让我们一起遇见更好的自己!