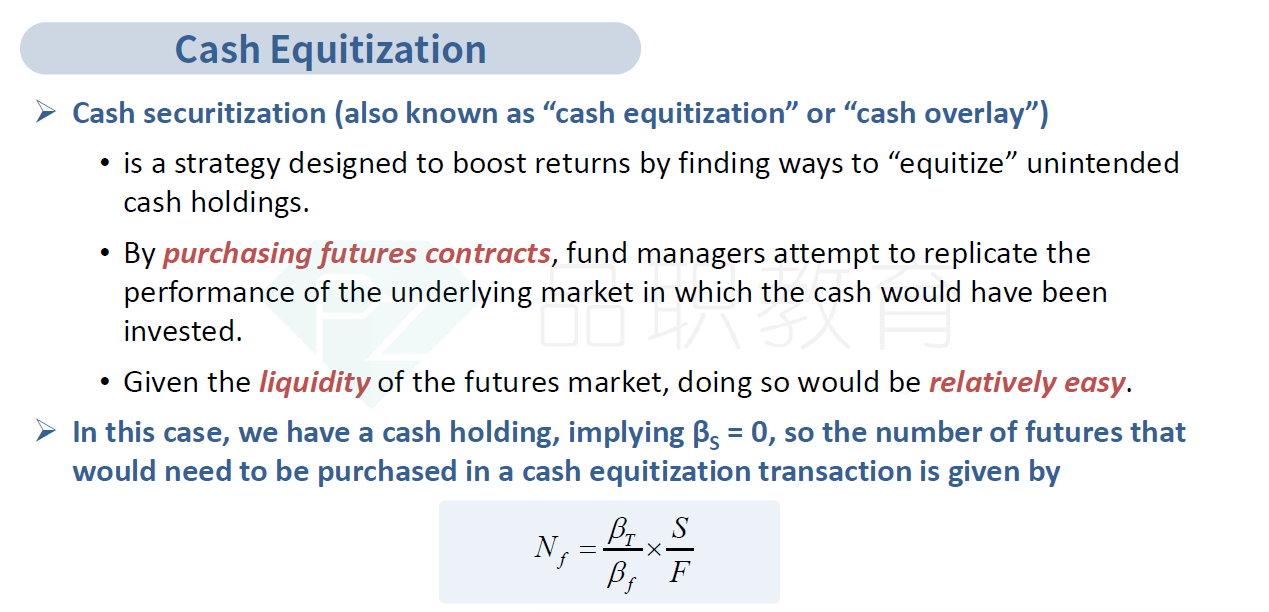

NO.PZ201601050100001703

问题如下:

The number of S&P 500 futures contracts that Whitacre should buy to equitize

Portfolio B’s excess cash position is closest to:

选项:

A. 6.

121.

1,455.

解释:

A is correct.

The number of equity index futures contracts to purchase in order

to equitize Monatize’s excess cash position is calculated as follows:

The actual futures contract purchase value of $825,000 is the product of the

quoted S&P 500 futures price of 3,300 and the designated multiplier of $250 per

index point.

中文解析:

根据题干意思可知,需要把多余的现金$4,800,000等效为持有标普500指数,因此需要将这部分cash的β调整到和标普500指数的β相同的数值。

其中标普500指数的β=1.cash的β=0. 因此βT =1.βP =0,带入上述公式就算结果为5.82份,四舍五入取整数为6份。

因此需要买入6份股指期货合约。

请问老师,要把多余的cash equitilize 掉,是把cash放在 资产方向还是target方向呀?因为我放在资产方向算出来是-5.82

4.8million+N×β(index)×Price(index)=0

如果是要放在target那边,应该怎么去理解呢?