NO.PZ201812020100000402

问题如下:

SD&R

Capital (SD&R), a global asset management company, specializes in fixed-income

investments. Molly, chief investment officer, is meeting with a prospective

client, Leah of DePuy Financial Company (DFC).

Leah

informs Molly that DFC’s previous fixed-income manager focused on the interest

rate sensitivities of assets and liabilities when making asset allocation

decisions. Molly explains that, in contrast, SD&R’s investment process first

analyzes the size and timing of client liabilities, and then it builds an asset

portfolio based on the interest rate sensitivity of those liabilities.

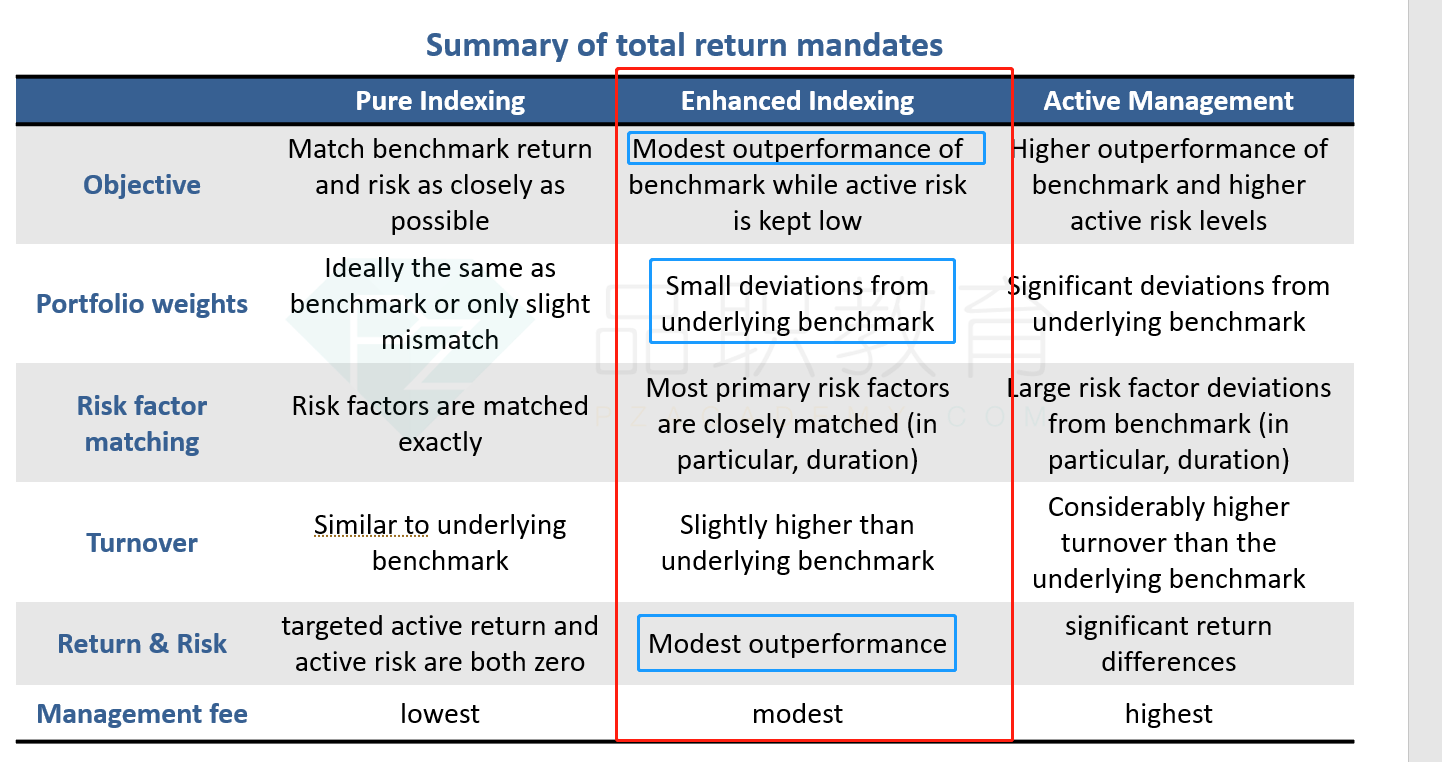

Molly notes that SD&R generally uses actively managed portfolios designed to earn a return in excess of the benchmark portfolio. For clients interested in passive exposure to fixed-income instruments, SD&R offers two additional approaches.

- Approach 1: Seeks to fully replicate a small range of benchmarks consisting of government bonds.

- Approach 2: Follows an enhanced indexing process for a subset of the bonds included in the Bloomberg Barclays US Aggregate Bond Index. Approach 2 may also be customized to reflect client preferences.

Leah informs Molly that DFC has a single $500 million liability due in nine years, and she wants SD&R to construct a bond portfolio that earns a rate of return sufficient to pay off the obligation. Leah expresses concern about the risks associated with an immunization strategy for this obligation. In response, Molly makes the following statements about liability-driven investing:

- Statement 1: Although the amount and date of SD&R’s liability is known with certainty, measurement errors associated with key parameters relative to interest rate changes may adversely affect the bond portfolios.

- Statement 2: A cash flow matching strategy will mitigate the risk from non-parallel shifts in the yield curve.

The discussion turns to benchmark selection. DFC’s previous fixed-income manager used a custom benchmark with the following characteristics:

- Characteristic 1: The benchmark portfolio invests only in investment-grade bonds of US corporations with a minimum issuance size of $250 million.

- Characteristic 2: Valuation occurs on a weekly basis, because many of the bonds in the index are valued weekly.

- Characteristic 3: Historical prices and portfolio turnover are available for review.

Relative to Approach 1 of gaining passive exposure, an advantage of

Approach 2 is that it:

选项:

A.minimizes tracking error.

requires less risk analysis

is more appropriate for socially responsible investors

解释:

C

is correct. Enhanced indexing is especially useful for investors who consider

environmental, social, or other factors when selecting a fixed-income

portfolio. Environmental, social, and corporate governance (ESG) investing,

also called socially responsible investing, refers to the explicit inclusion or

exclusion of some sectors, which is more appropriate for an enhanced index

strategy relative to a full index replication strategy. In particular, Approach

2 may be customized to reflect client preferences.

前面有老师回答:tracking error=active return/active risk。用来衡量主动管理的active return(Rp-Rb)的波动程度,tracking error越大,表明portfolio的收益与benchmark收益deviation的越大,所以,主动管理的程度越高。明白了这一点,从tracking error的角度,pure index<enhance indexing<active management。pure index基本没有tracking errer。

之前做过一道类似的题,答案并不是完全复制的tracking risk 最小,因为还要考虑交易费用和其他成本。