NO.PZ2023020101000013

问题如下:

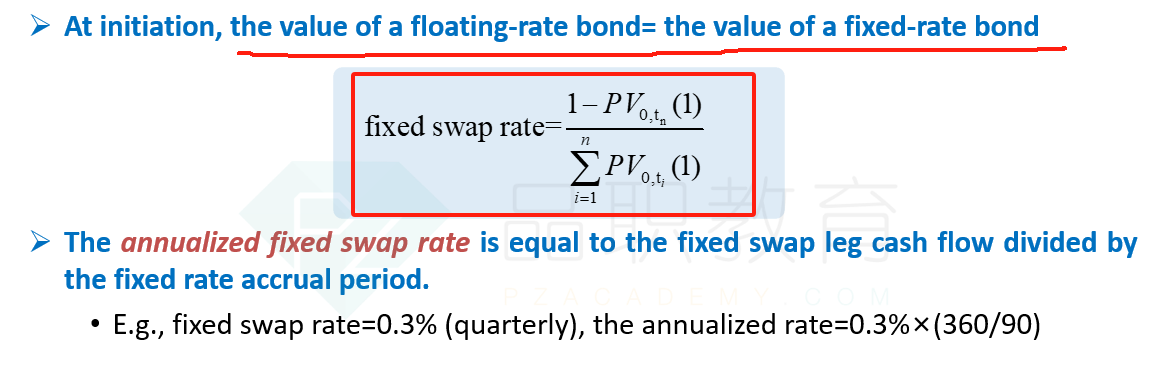

Yang asks Whitney to explain the

calculation of the fixed swap rate in a floating-for-fixed interest rate swap.

Whitney outlines three possible methods for Yang to consider.

•

Method 1 The swap rate is the difference between MRR

and the fixed interest rate on the bond.

•

Method 2 The swap rate is the rate that sets the

value of the fixed-rate bond equal to the notional principal of the swap.

•

Method 3 The swap rate is the rate that sets the

initial value of the swap equal to zero.

Which method described by Whitney is most

likely correct?

选项:

A.Method

3

Method

2

C.

Method

1

解释:

A is

correct. The swap rate in a fixed-for-floating swap is the fixed rate that sets

the initial value of the swap equal to zero. This is accomplished by setting

the value of the fixed side equal to that of the floating side.

The swap rate is the rate that sets the value of the fixed-rate bond equal to the notional principal of the swap.

不是根据“NP=coupon折现+NP折现”算出fixed rate的吗?

那这个表述错在哪里呢?“the value of the fixed-rate bond”指的是什么?