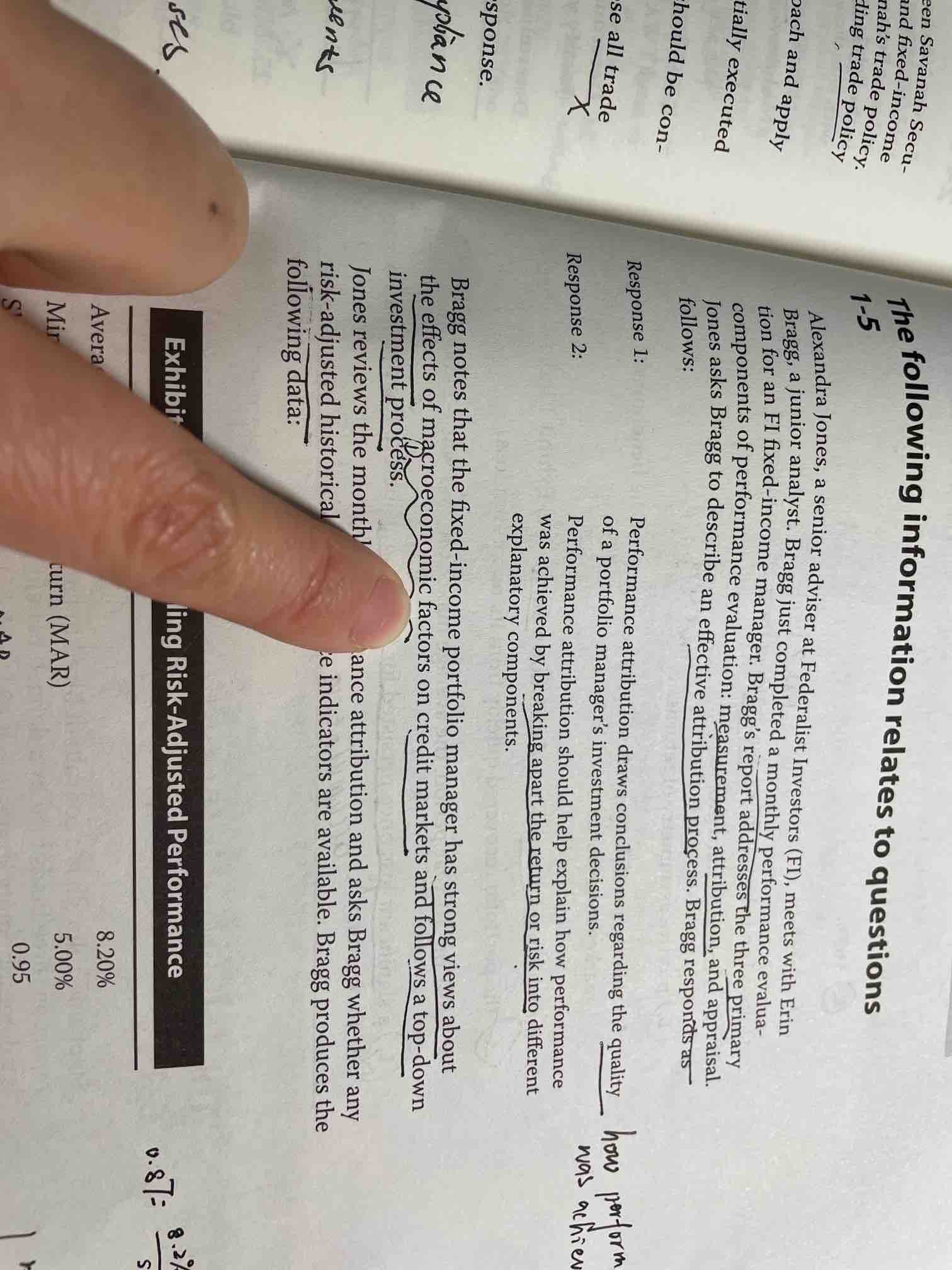

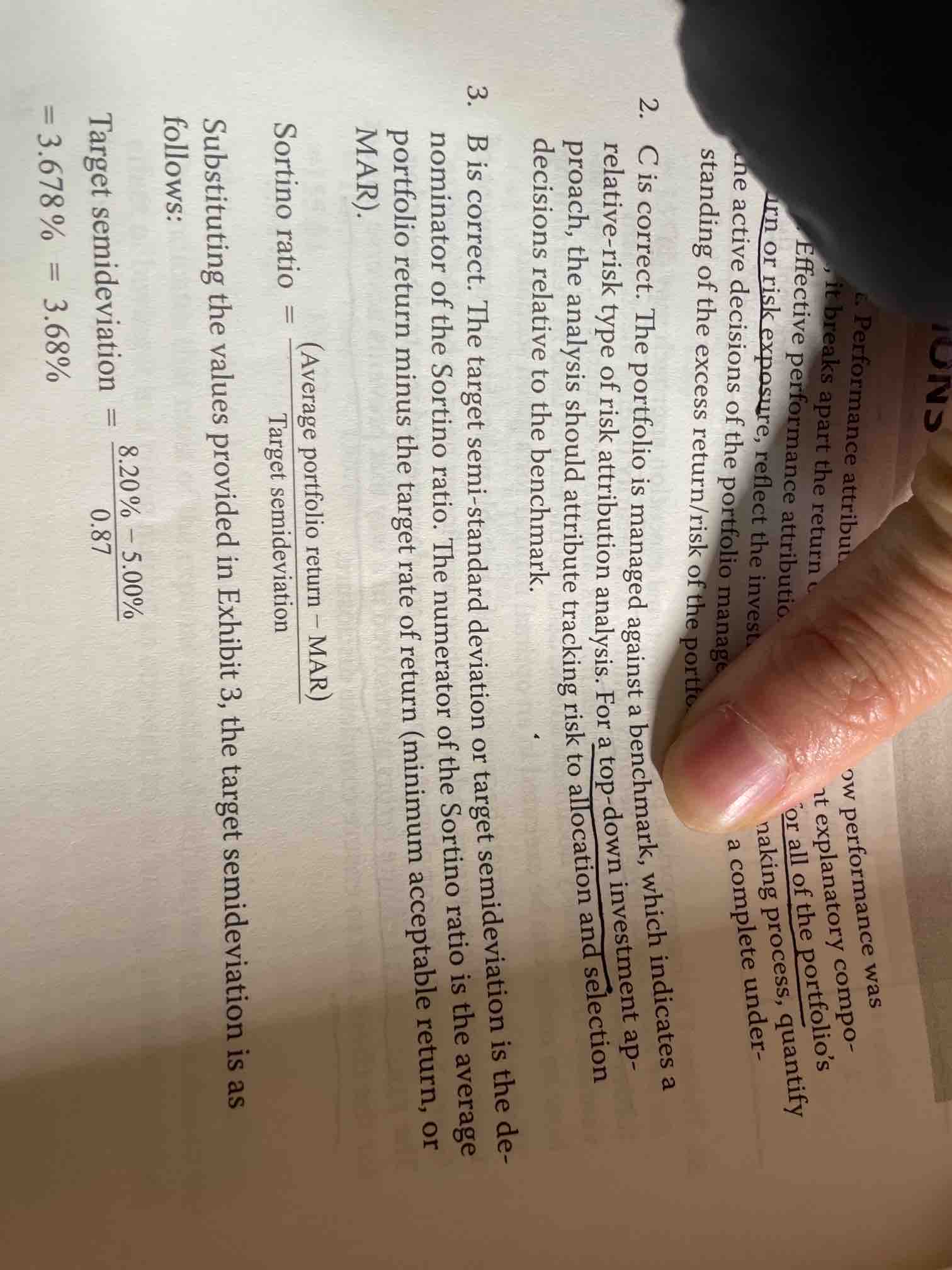

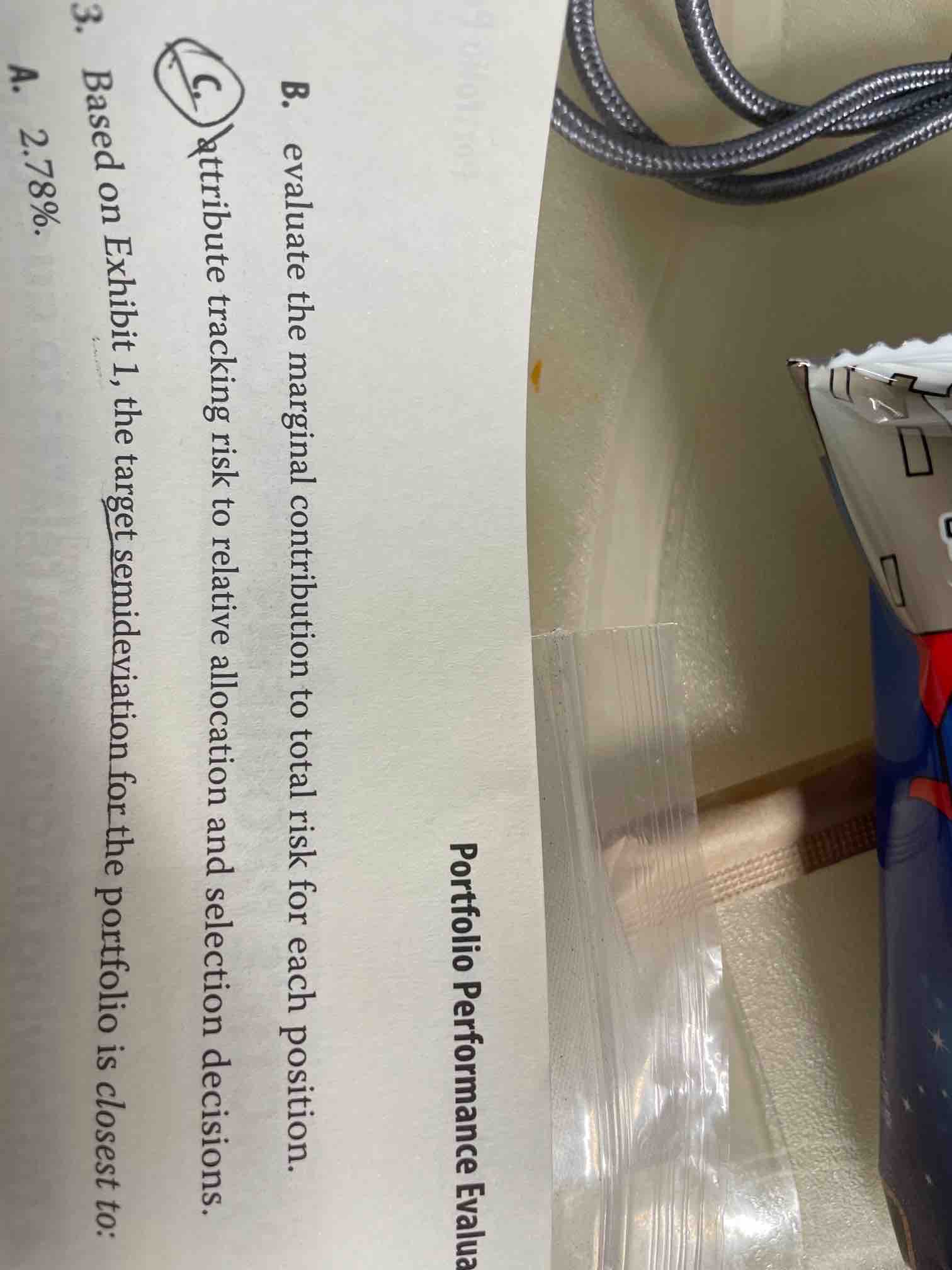

1、这题为什么不选A呢?2、 解析说它是relative的,从哪里看出relative了呢? 看题应该是factor based,因为分析师有一个strong view about macro factor

吴昊_品职助教 · 2024年02月01日

嗨,努力学习的PZer你好:

题干并没有说benchmark,答案解析跑上来就说against a benchmark确实属于无厘头了,这是原本书的bug。所以我们只能通过排除法来进行选择。

A选项说的是分解return(decompose historical returns),这和题干risk attribution不符。

B选项错在最后“each postion”,top-down方法不能是each postion,这是bottom-up方法对应的描述。

----------------------------------------------虽然现在很辛苦,但努力过的感觉真的很好,加油!