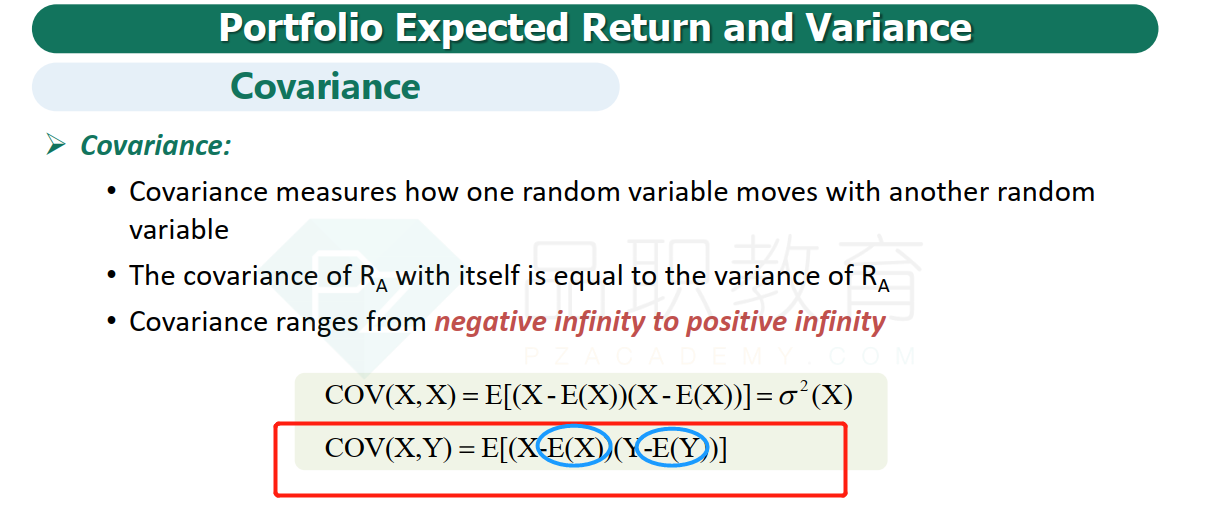

NO.PZ2022123001000053

问题如下:

The joint probability of returns, for securities A and B, are as follows:

The covariance of the returns between securities A and B is closest to:

选项:

A.3%2

12%2

24%2

解释:

Expected return on

security A= 0.6 x 25% + 0.4 x 20% = 15% + 8% = 23%

Expected return on security B= 0.6 x 30% + 0.4 x

20% = 18% + 8% = 26%

Cov

(RA, RB) = 0.6 [(25% - 23%)(30% - 26%)] + 0.4 [(20% -

23%)(20% - 26%)] = 0.6 (2% x 4%) + 0.4 (-3% x -6%)= 12%2

expected return 的公式不是w乘以expected return就可以了么?未什么还要减去expe return?