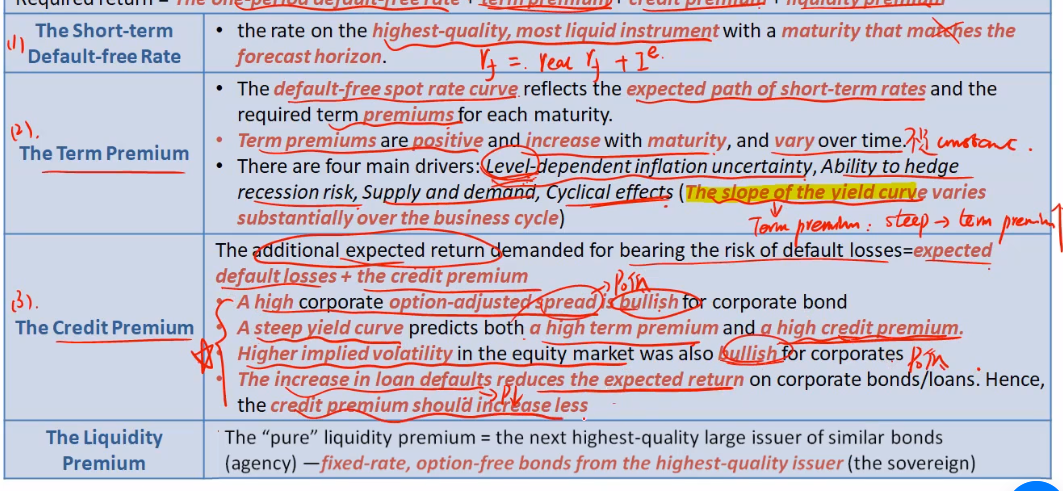

The increase in loan defaults reduces the expected return on corporate bonds/loans. Hence, the credit premium should increase less. 这句话怎么理解 麻烦再讲一下。

这里说的loan defaults是指某一个特定的loan还是说市场上整体贷款违约率变高?

是否是说如果买了一个债券违约了,那就这只债券本身的expected return就降低了,所以credit premium也一同降低了?