NO.PZ2023103101000060

问题如下:

Q. A common problem for the “mark-to-model” valuation of private equity funds is most likely:选项:

A.a violation of accounting rules. B.an understatement of portfolio risk. C.an understatement of interim portfolio return.解释:

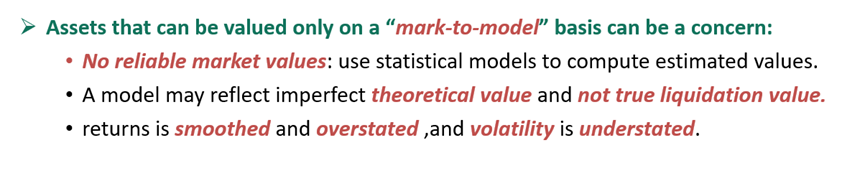

B is correct. Accounting rules require that investments be recorded at their fair value for financial reporting purposes. The fair value of private equity that owns illiquid assets requires certain estimates, rather than observable transaction prices, to be factored into valuation. A model that relies on Level 3 inputs may reflect an imperfect theoretical valuation and not a true liquidation value. The lack of new market information over time may anchor the interim valuation at or near initial cost. The relatively stable accounting valuations may give investors a false sense that they are less volatile. At the same time, there is a potential conflict of interest for the GP to overstate interim return because of the implication for carried interest. As a result, returns may be smoothed or overstated and the volatility of returns understated.

为什么选b呢,是哪个知识点