NO.PZ202208260100000402

问题如下:

A Baywhite client currently owns 5,000 common non-dividend-paying shares of Vivivyu Inc. (VIVU), a digital media company, at a spot price of USD173 per share. The client enters into a forward commitment to sell half of its VIVU position in six months at a price of USD175.58. Which of the following market events is most likely to result in the greatest gain in the VIVU forward contract MTM value from the client's perspective?

选项:

A.An increase in the risk-free rate

B.An immediate decline in the VIVU spot price following contract inception

C.A steady rise in the spot price of VIVU stock over time

解释:

Solution

B is correct.

The original VIVU spot price (S0) at t = 0 must equal the present value of the forward price discounted at the risk-free rate, so an immediate fall in the spot price to S0- < S0 results in an MTM gain for the forward contract seller. A is not correct, since a higher risk-free rate will reduce the contract MTM from the client's perspective by reducing the PV of F0(T), while C will also reduce the forward contract MTM from the seller's perspective.

中文解析:

根据题干可知,客户想要通过远期合约在六个月后减少持有的股票头寸,因此他应该进入的是short

forward头寸。

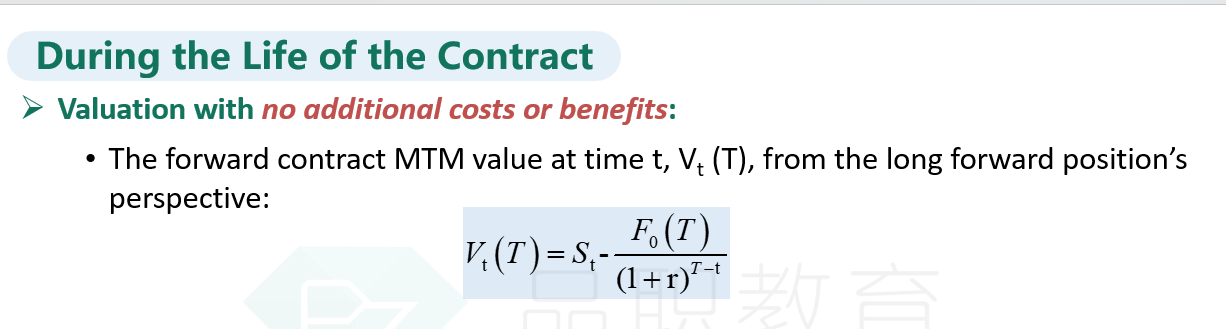

Short forward头寸下,MTM

value = F0(T)/(1+r)T-t - St

由上式可以看到:无风险利率上涨,以及股票价格上涨,都会使得MTM

value下降。而股票价格下跌,会使得MTM

value上涨。因此选B。

老师,这个 short forward 的公式是什么,在讲义哪里?