NO.PZ201809170400000203

问题如下:

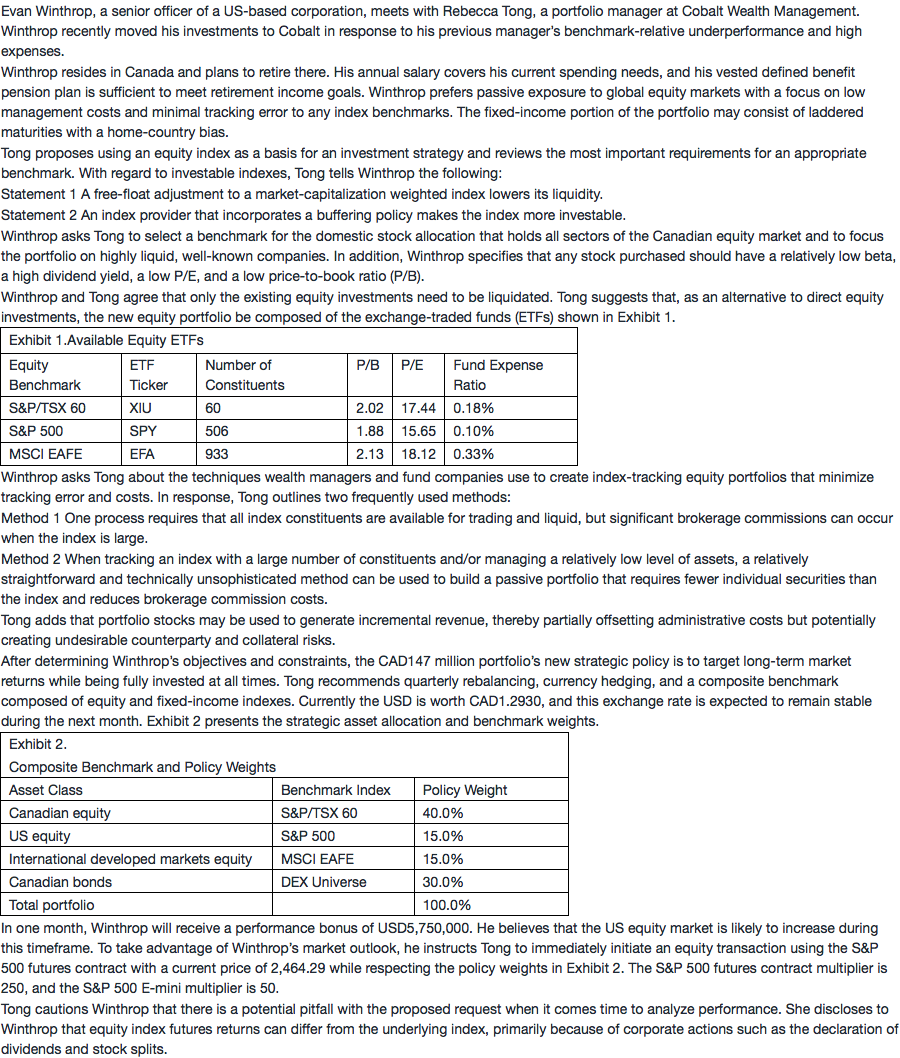

Based on Exhibit 1 and assuming a full-replication indexing approach, the tracking error is expected to be highest for:

选项:

A.

XIU.

B.

SPY.

C.

EFA.

解释:

C is correct. An index that contains a large number of constituents will tend to create higher tracking error than one with fewer constituents. Based on the number of constituents in the three indexes (S&P/TSX 60 has 60, S&P 500 has 506, and MSCI EAFE has 933), EFA (the MSCI EAFE ETF) is expected to have the highest tracking error. Higher expense ratios (XIU: 0.18%; SPY: 0.10%; and EFA: 0.33%) also contribute to lower excess returns and higher tracking error, which implies that EFA has the highest expected tracking error.

有助教回答说是这道题应该从指数的角度出发,指数里包含的股票越多越难复制,但是另一个助教回答说这是指fund持股,s&p500里不可能是506只股票,所以到底该从哪个角度理解呢,还是没搞明白,谢谢