NO.PZ202207040100001006

问题如下:

Which comment by Parker regarding factor-based approaches is most accurate? The comment regarding:

选项:

A.

value factor funds.

B.

single-factor funds.

C.

fundamental weighting.

解释:

B is correct. Relative to cap weighting, single-factor funds concentrate risk exposure to the characteristics of the factor used.

A is incorrect. Value factor funds focus on valuation measures, not volatility.

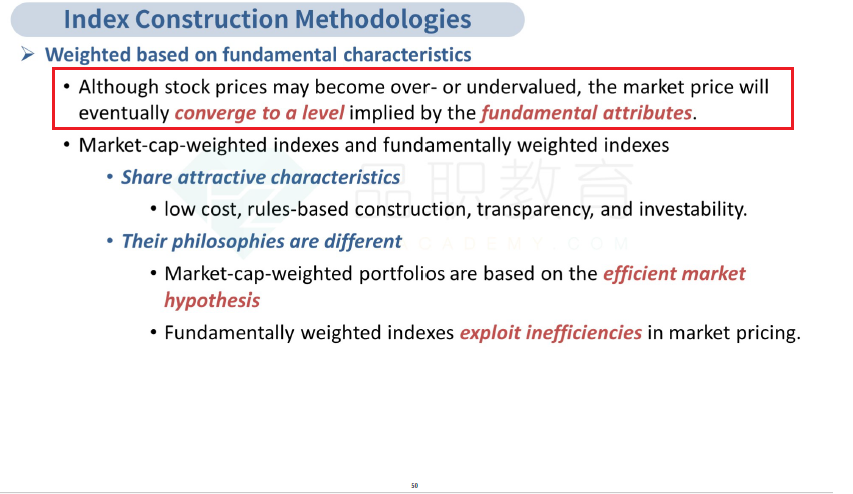

C is incorrect. Fundamental weighting’s intended advantage is overweighting stocks priced below intrinsic value and underweighting overpriced stocks.

老师,fundamental weighting是怎么做的,不是选基本面指标好的吗,那跟intrinsic value的计算有什么关系呢