NO.PZ202305230100005404

问题如下:

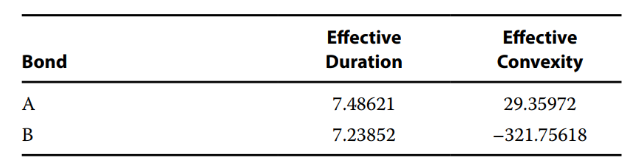

For the percentage price change for Bond A, given a 200 bp increase in benchmark yield, what part of the price change is of the most concern?

选项:

A.

Duration

B.

Convexity

C.

Not able to determine with given information

解释:

A is correct. Typically, the effect of duration is much larger than the effect of convexity.

%∆PVFull Bond A, Duration ≈ –7.48621 × 0.0200 = –14.97242%

%∆PVFull Bond A, Convexity Adjustment ≈ 0.5 × 29.35972 × (–0.0200)^2 = –0.58719%

计算数据哪来的呢?题干没有呀