NO.PZ2023101601000064

问题如下:

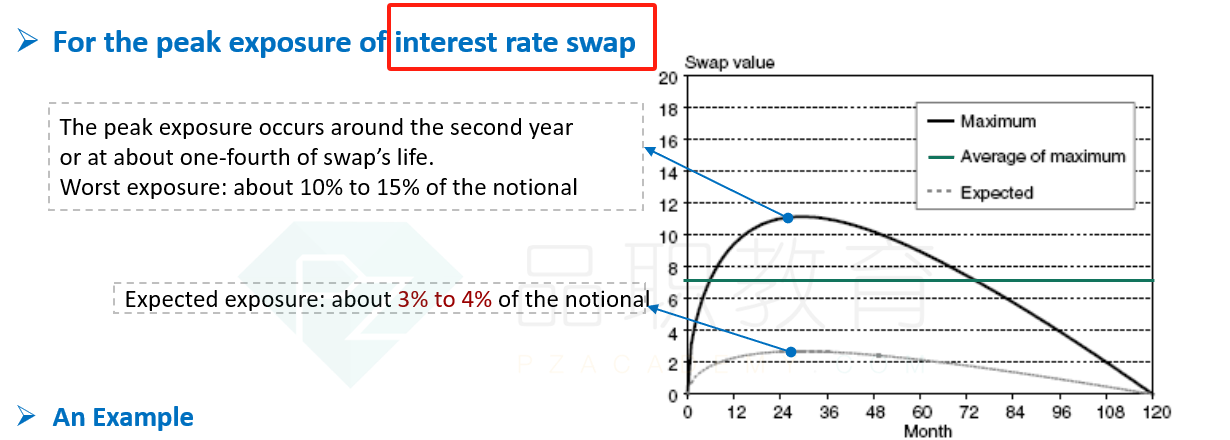

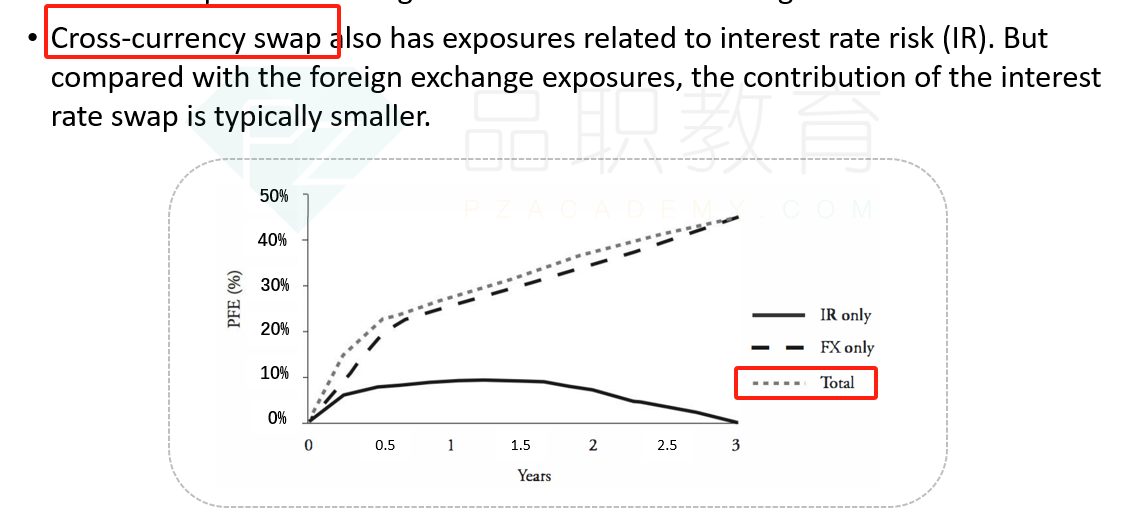

The chart below shows three exposure profiles, where the exposure metric is the potential future exposure (PFE): PFE of an interest rate swap (IRS), PFE of a foreign exchange (FX) forward contract, and PFE of a cross-currency swap. Also plotted is the average PFE of the interest rate swap, where "average PFE" is what Jorion calls the average worst credit exposure (AWCE). Which position's (instrument's) exposure profile is most likely the uppermost, concave plot line?

选项:

A.

PFE of interest

rate swap

B.

PFE of foreign

exchange (FX) contract

C.

PFE of

cross-currency swap

D.

Average PFE of

interest rate swap

解释:

PFE of cross-currency

swap, which combines the exposure of an interest rate swap and the FX forward.

The dotted must be the average PFE (aka, AWCE) since it is a flat line.

老师您好,请问这是哪个知识点里面的内容呀?可以解释一下这道题嘛?谢谢老师