NO.PZ2023101601000137

问题如下:

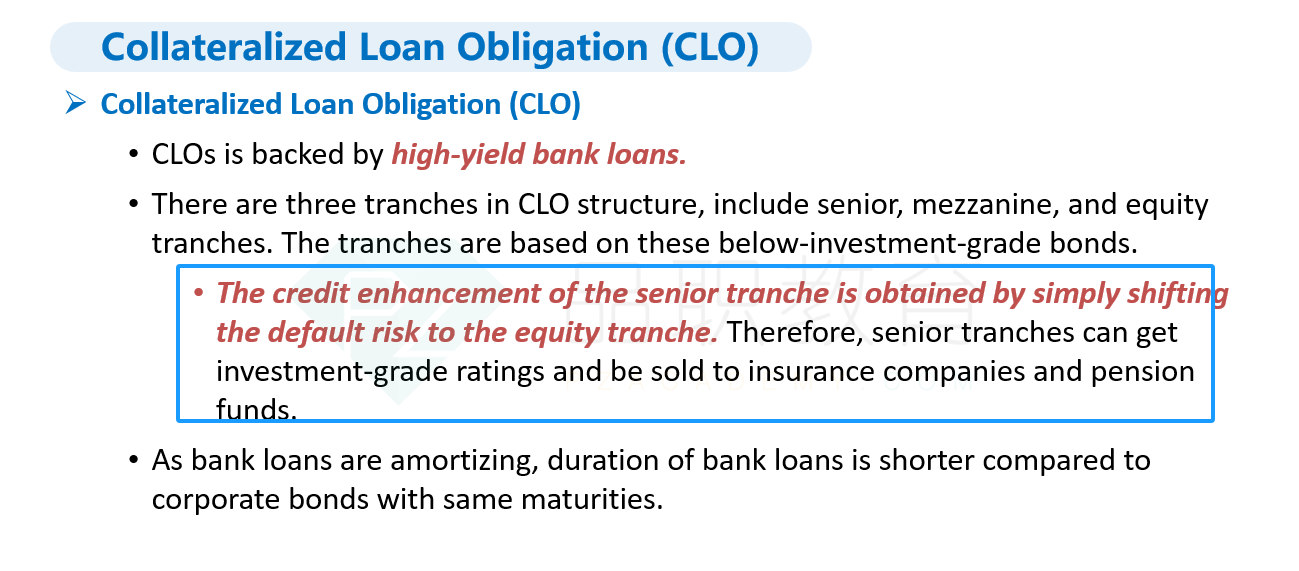

An underwriter structures a

collateralized loan obligation(CLO) composed of 100 identical loans, each with

a notional value of GBP 800,000 to be repaid in one year with an interest rate

of LIBOR + 3%.The CLO has one planned payment at maturity and its capital

structure is given by:

At maturity the CLO accumulates GBP 6,625,000 of

losses from defaults and unpaid interest. If LIBOR was flat at 1% over the

1-year period, and assuming no recovery on the defaults, how would the losses

be absorbed by the capital structure?

选项:

A.

The

equity tranche will lose some of its value, and the other tranches will not be

affected.

B.

The

equity tranche will lose all of its value, and the other tranches will not be

affected.

C.

The

equity tranche will lose some of its value, and the mezzanine tranches will

lose some of its value.

D.

The

equity tranche will lose all of its value, and the mezzanine tranche will lose

some of its value.

解释:

老师您好,请问这是哪个知识点里面的内容呀?可以解释一下这道题嘛?谢谢老师