NO.PZ202305230100009002

问题如下:

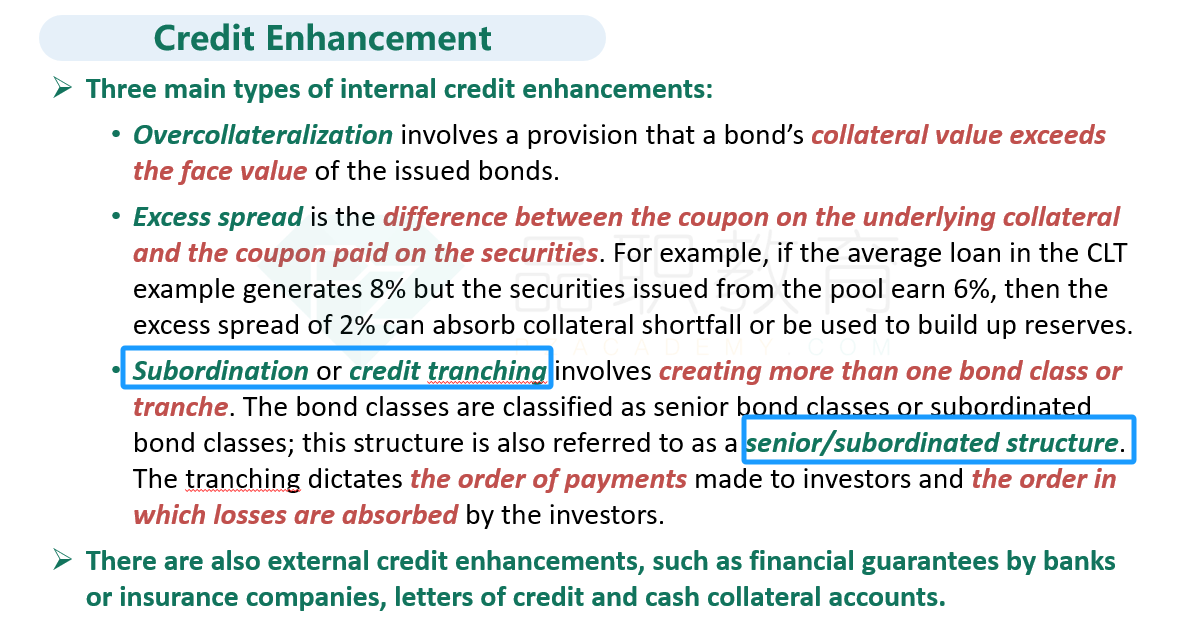

Select which of the following statements related to the collateralized bonds issued directly by the SPE is most accurate.

选项:

A.This senior/subordinated structure is an example of time tranching.

Losses are realized by the subordinated bond classes before any losses are realized by Class A bonds.

C.In a waterfall structure such as this one, losses are shared proportionally across all subordinated bond classes.

解释:

The correct answer is B. Losses are realized by the subordinated bond classes before any losses are realized by the senior Class A bonds. A is incorrect because this senior/subordinated structure is an example of credit tranching, not time tranching. C is incorrect because in a waterfall structure such as this one, the most junior tranche, Class D, will absorb all losses up to its full CAD50 million par value first. Then, if credit losses exceed that threshold, Bond Class C will absorb all losses up to its full CAD100 million par value. The losses are not shared proportionally across all subordinated bond classes; instead, they are absorbed by the most junior classes first and subsequently by the more senior ones up to the value of the loss.

a为什么不是time tranching啊