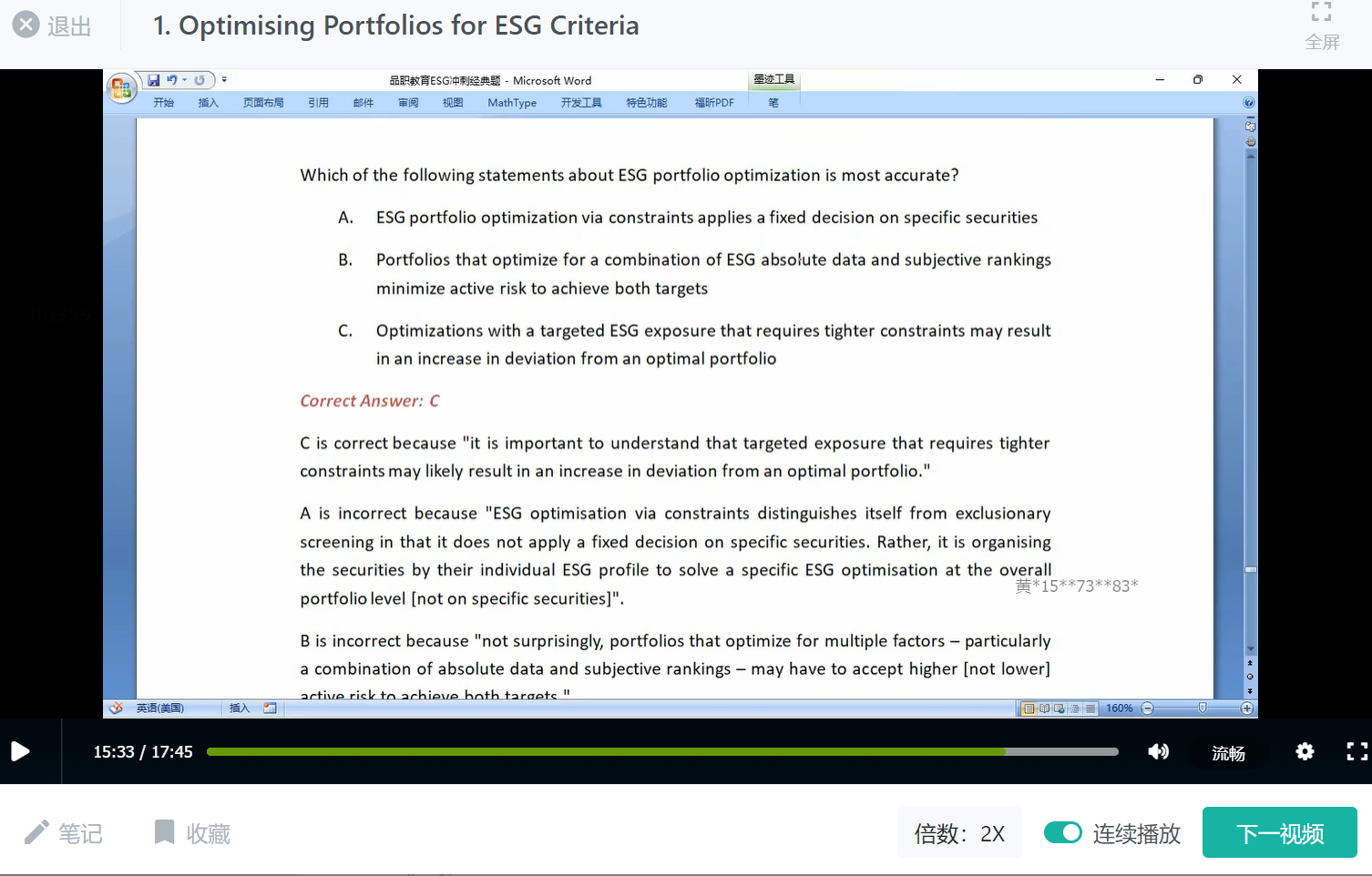

1.2 Which of the following statements about ESG portfolio optimization is most accurate? (V4

Mock#91)

..

AB

C.

ESG portfolio optimization via constraints applies a fixed decision on specific securities

Portfolios that optimize for a combination of ESG absolute data and subjective rankings

minimize active risk to achieve both targets

Optimizations with a targeted ESG exposure that requires tighter constraints may result

in an increase in deviation from an optimal portfolio

Correct Answer: C