NO.PZ2023101601000028

问题如下:

A fixed-income

portfolio analyst is calculating the i-spread on a 10-year, 3.5% fixed-rate

USD-denominated bullet bond issued by Bank TBT. The bond is currently rated A-,

has no embedded options, makes semi-annual payments, and has 4.5 years

remaining to maturity. The analyst obtains the following information:

Yield to maturity of the bond: 4.67%

Yield on the nearest-maturity on-the-run Treasury note: 1.15%

Yield on a 4-year Treasury note: 1.65%

Yield on a 5-year Treasury note: 2.08%

The linearly interpolated 4.5-year swap rate: 1.94%

The z-spread: 316 bps

What is the i-spread on the

bond?

选项:

A.151bps

B.273bps

C.352bps

D.431bps

解释:

B is correct. The

i-spread is the difference between the interpolated yield and the yield on the

credit-risky bond = 4.67 – 1.94 = 2.73% = 273 bps.

A is incorrect. 151

bps is the difference between the yield to maturity of the bond and the z

spread.

C is incorrect. 352

bps is the bonds yield spread.

D is incorrect. 431

bps is the result of adding the z-spread to the yield on the nearest maturity

on-the-run Treasury note.

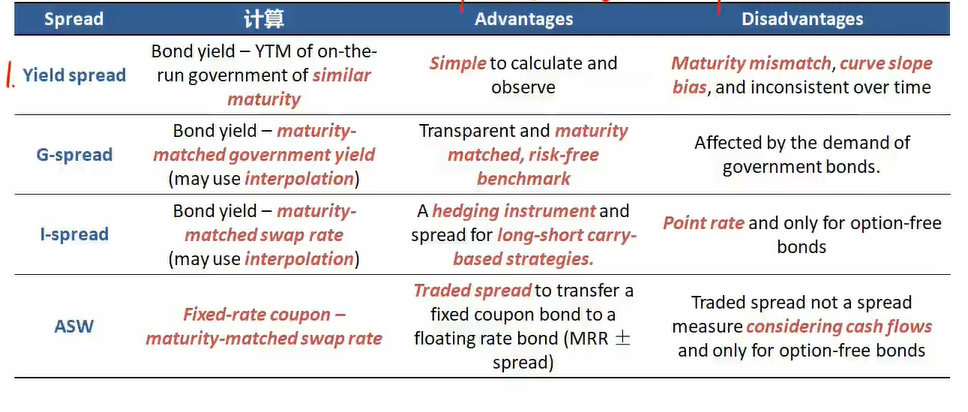

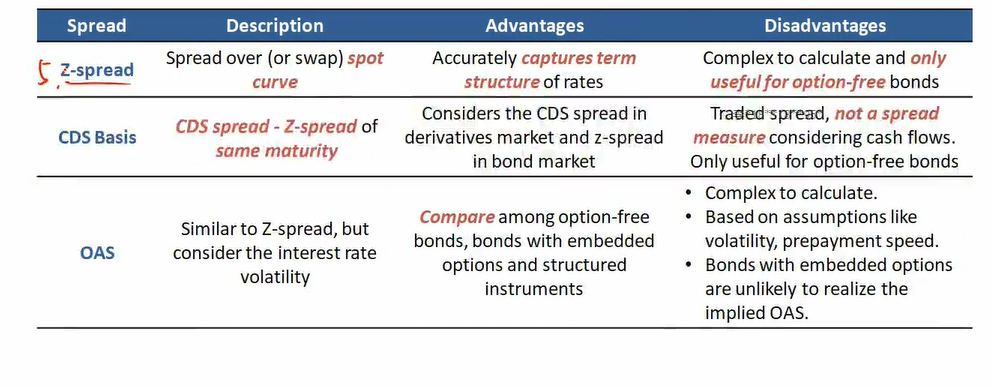

如标题,回翻课件找不到相关的内容了。一级似乎学过nominal-s,z-s和oas,但是记录的不太清晰,分不清楚都是哪些因子作差。再加上本题里面提到的几种spread。请老师帮忙总结一下。