NO.PZ202208300100000903

问题如下:

The new accounting policy adopted in 2016 for the customer acquisition cost related to long-term wireless contracts (Exhibit 3, Note 1 d) most likely increases CCCL’s:

选项:

A.quality of earnings.

B.cash from operations.

C.debt to asset ratio.

解释:

Solution

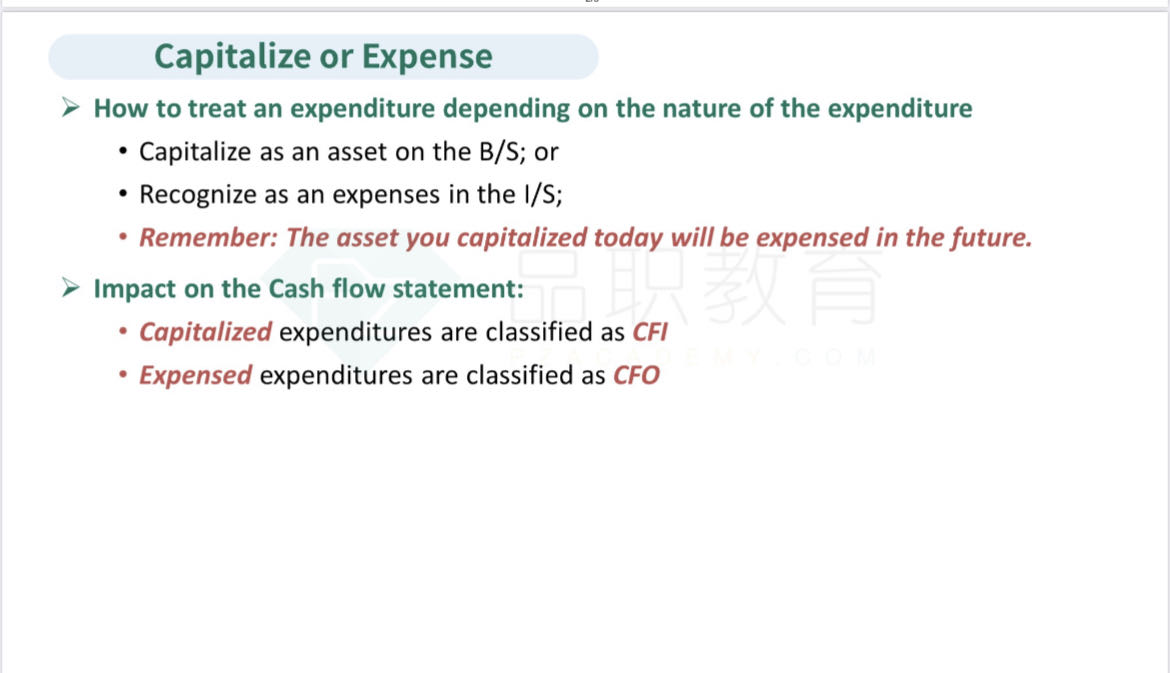

B is correct. In 2016, CCCL started capitalizing the discount offered (from selling the mobile devices at a lower price) instead of recording it in the period it is incurred. This change in the policy would increase net income (by lowering expenses) and cash from operations. The amounts capitalized would be recorded as cash outflows for investing activities, compared to cash from operations if they were expensed.

C is incorrect. The total assets would increase by the amount capitalized (as opposed to expensed) (be higher) hence the D/A ratio would decrease.

A is incorrect. Capitalizing decreases the quality of earnings because it would be more conservative and closer to cash flow to expense the losses in the period. The future benefit and the ability to match these costs to revenues are uncertain, particularly given CCCL’s new policy to accelerate the recognition of revenue on long-term contracts.

中文解析:

这道题考查的是财务报告的质量潜在问题:分类问题。

题干给了,2015年底,cccl收购了该无线部门。该公司希望审查cccl对长期无线合同的收入和费用所采取的会计政策。注1d:签订无线服务长期服务合同的客户可以以名义金额获得他们的移动设备。从2016年开始,设备相对于正常价格的折扣被资产化为客户的获取成本,并在合同有效期内或至少三年内直线摊销。以前,这一数额立即计入I/S中。

接下来题目问,与长期无线合同(表3,注1d)相关的客户获取成本2016年采用新的会计政策最有可能增加了CCCL的哪个指标。

分类问题主要是指不按经济实质对报表项目进行错误分类,从而误导报表使用者。比如将营业外收入确认为经营收入,高估可持续性利润;或者将不满足资本化条件的费用资本化,以降低当期费用,提高当期净利润。本题中的情况主要是费用资本化。B选项是正确的。2016年,CCCL开始把优惠的折扣(从以较低的价格出售移动设备)资本化,而不是在折扣发生期间就直接计入费用中。政策的改变将增加净收入(通过降低费用)和经营性现金。资本化的金额将计入投资活动的现金流出,而不是经营性现金的支出。

A选项是错误的。资本化会降低收益的质量,因为资本化把收益变得更加不保守。未来将这些成本与收入相匹配的能力是不确定的,特别是考虑到CCCL的新政策是加速确认了长期合同产生的收入。

C选项是错误的。总资产中增加了资本化金额,因此总资产变大,因此D/A比率将下降。

为什么net income 增加 就会增加 cash from operations?原价卖100元,现价卖90元,原来10元记在损益表的成本或费用里。现在10元分N年摊销,最低3年,当年最多记3.3元,利润是增加了,但是现金并没有啊?