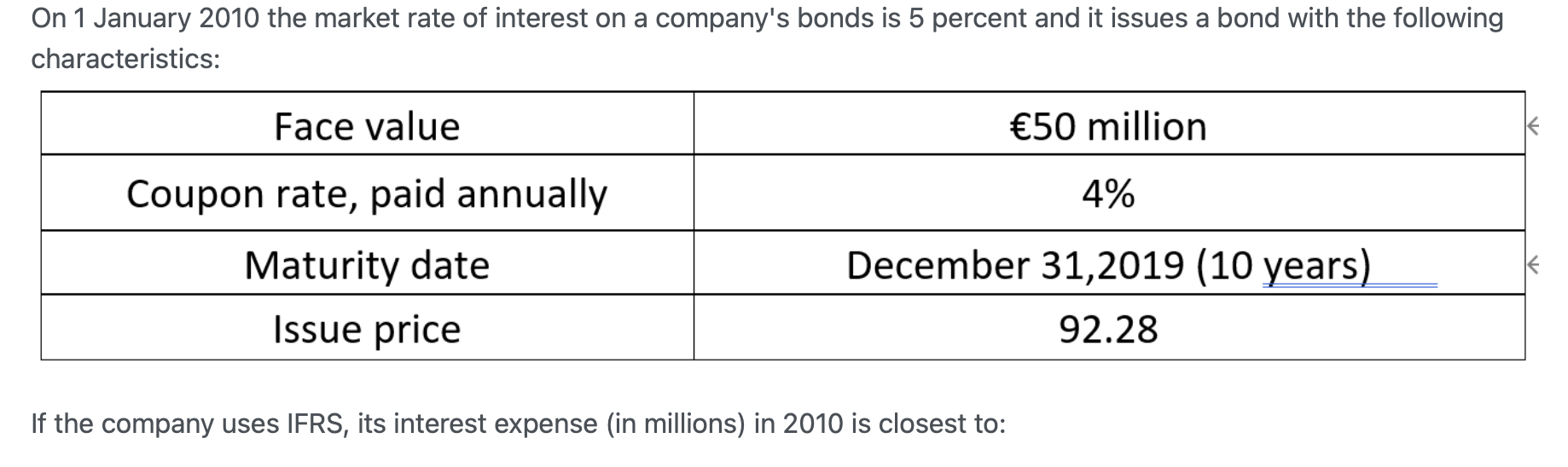

NO.PZ2023020602000193

问题如下:

A company had the following events related to $5 million of 10-year bonds with a coupon rate of 8% payable semiannually on 30 June and 31 December:

- Issued on 1 January 2005, when the market rate of interest was 6%.

- Bought back in an open market transaction on 1 January 2011, when the market rate of interest was 8%.

选项:

A.$346,511 gain on the income statement. B.$743,873 gain on the income statement. C.$350,984 decrease in the cash from operations.解释:

The book value of the bonds on 1 January 2011 is equal to the present value of the remaining coupon payments and principal discounted at the market rate at time of issue (3% per period).

Coupon = 0.08×0.5×5,000,000 = 200,000; there are 4 years remaining or 8 coupon payments.

Book value = 200,000 PV Annuity (n = 8; i = 3%) + 5.000,000 PV (n = 8; i = 3%)= 1,403,938 + 3,947,046 = 5,350,984

Using a financial calculator PMT = 200,000; FV = 5,000.000; (I % = 3%; N = 8);Compute PV = 5,350,984

Because the market interest rate when the bonds are bought back (8%) is equal to the coupon rate, the company can buy back the bonds at par $5,000,000.

On the cash flow statement the gain would be deducted from net income in calculating the cash from operations under the indirect method, and the cash paid to repurchase the bonds would be a cash outflow in the financing section.