NO.PZ2023091601000080

问题如下:

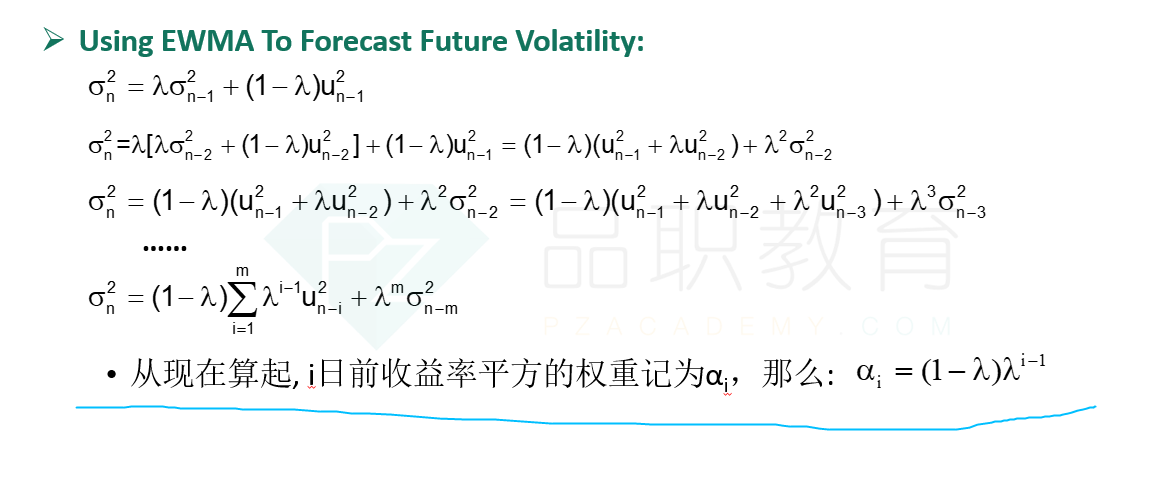

In

the EWMA model, the half-life is defined as the time, T, at which λT

= 1/2, where λ is the decay factor of the EWMA model. A risk analyst is using a

specific EWMA model to calculate volatility and determines that the half-life

of the model is 23 days. Based on the above information, which weight will be

applied to the return that is five days old?

选项:

A.0.026

0.031

0.781

0.859

解释:

如题