NO.PZ2018091706000048

问题如下:

Analyst Bob is studying foreign exchange market. He observes that:

1. The spot exchange market rate is 1.5500 USD/GBP

2. The 6-month Libor for dollars is 0.58, while the 6-month Libor for pounds is 0.62

So, Bob wants to calculate the USD/GBP exchange rate in 6 months but he finds that the forward currency contracts are not available. Which international parity condition should he use?

选项:

A.

Uncovered interest rate parity.

B.

Both covered interest rate parity and Uncovered interest rate parity.

C.

Covered interest rate parity.

解释:

A is correct.

考点:Interest rate parity

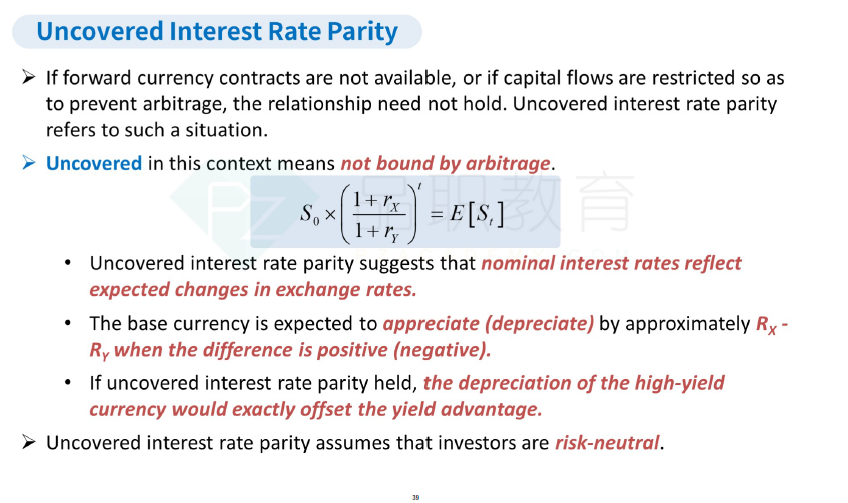

解析:解题的关键在与题目中一句话"the forward currency contracts are not available."这就表明因为没有远期合约的参与,所以没有套利机制保证covered interest rate parity成立,所以这时只能选用Uncovered interest rate parity。

老师时间久了真的彻底一点印象都没有,在哪个里回看?