NO.PZ2023091701000080

问题如下:

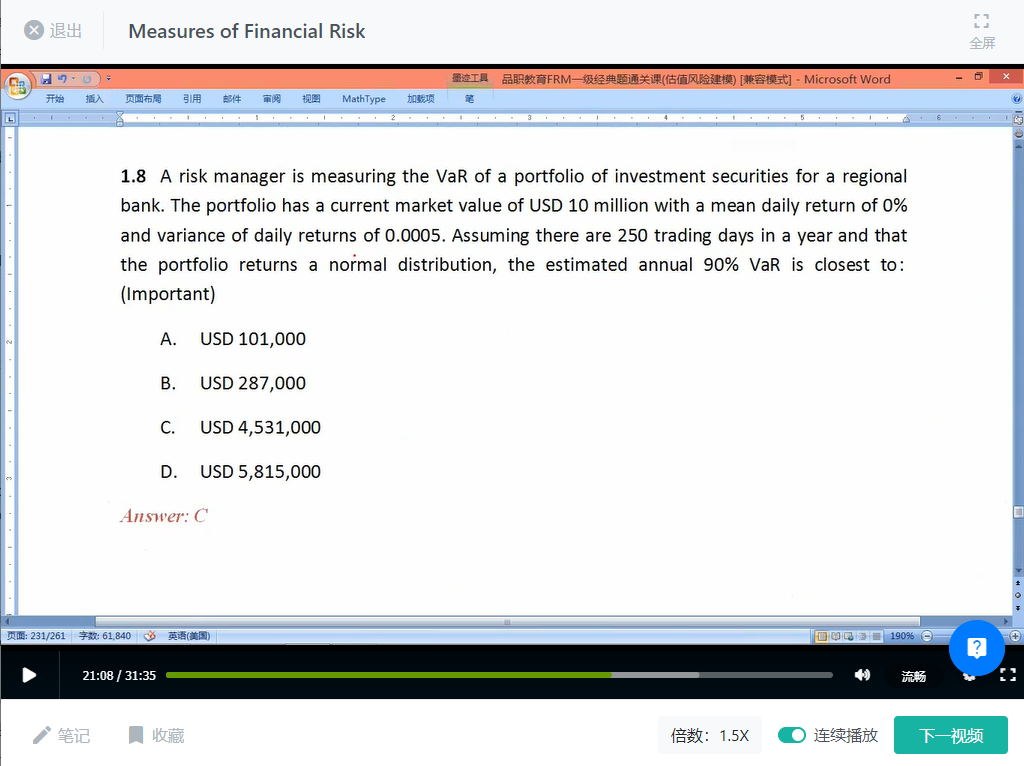

A risk analyst is asked to calculate the 1-day 99% VaR of a portfolio as well as to estimate the number of daily exceedances that are expected over the next year. Assuming 250 trading days in a year, what is the expected number of days of exceedances for this model within a year?

选项:

A.USD 101,000 B.USD 287,000 C.USD 4,531,000 D.USD 5,815,000解释:

如题