NO.PZ2023091802000130

问题如下:

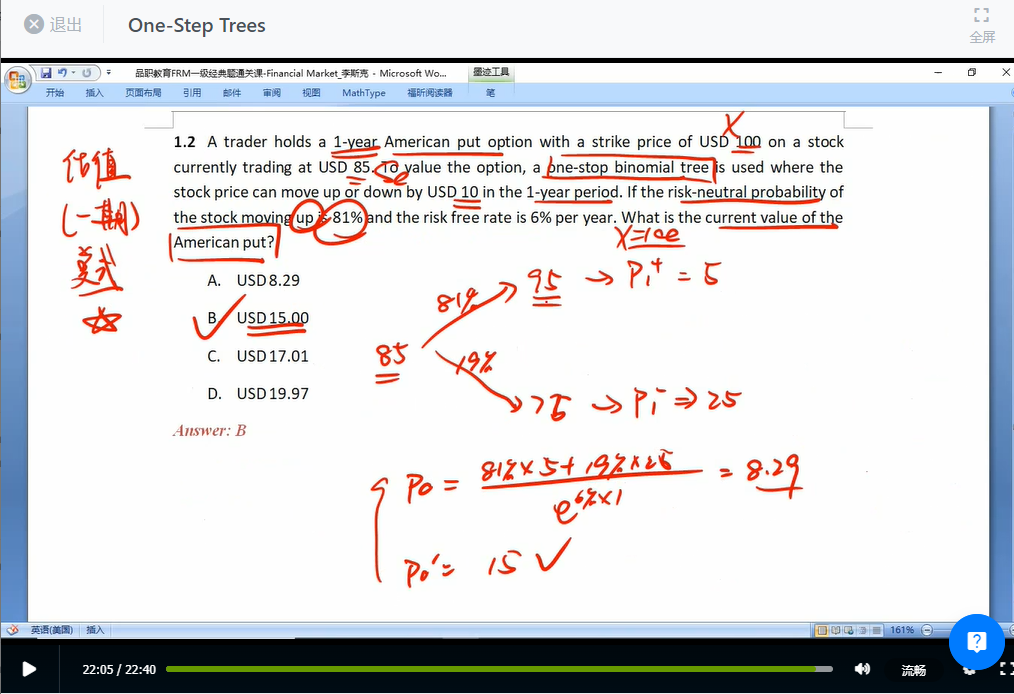

A trader holds a 1-year American put option with a strike price of USD 100 on a stock currently trading at USD 85. To value the option, a one-stop binomial tree is used where the stock price can move up or down by USD 10 in the 1-year period. If the risk-neutral probability of the stock moving up is 81% and the risk free rate is 6% per year. What is the current value of the American put?

选项:

A.USD 8.29

B.USD 15.00

C.USD 17.01

D.USD 19.97

解释:

求此题的计算过程