NO.PZ2019010402000061

问题如下:

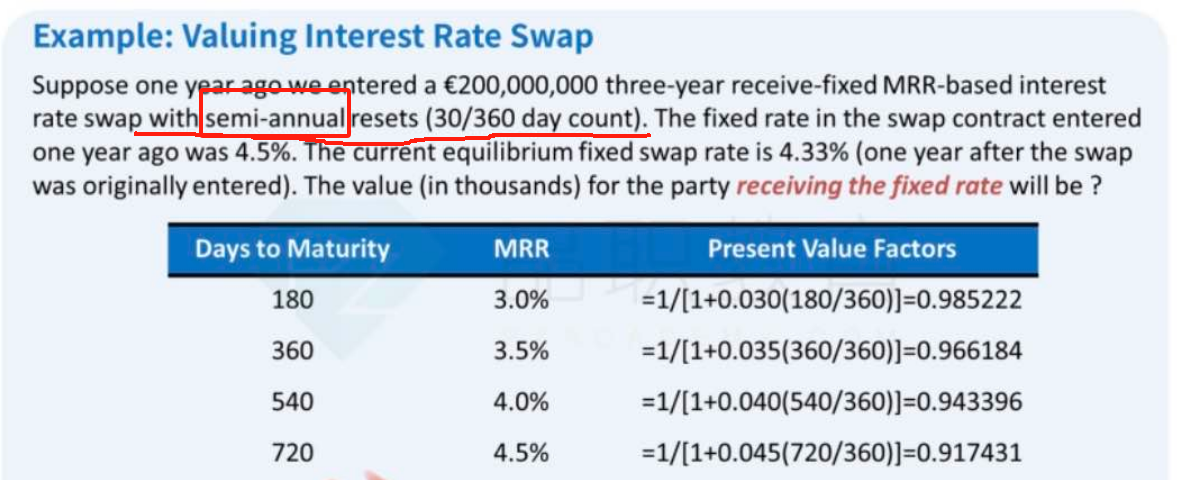

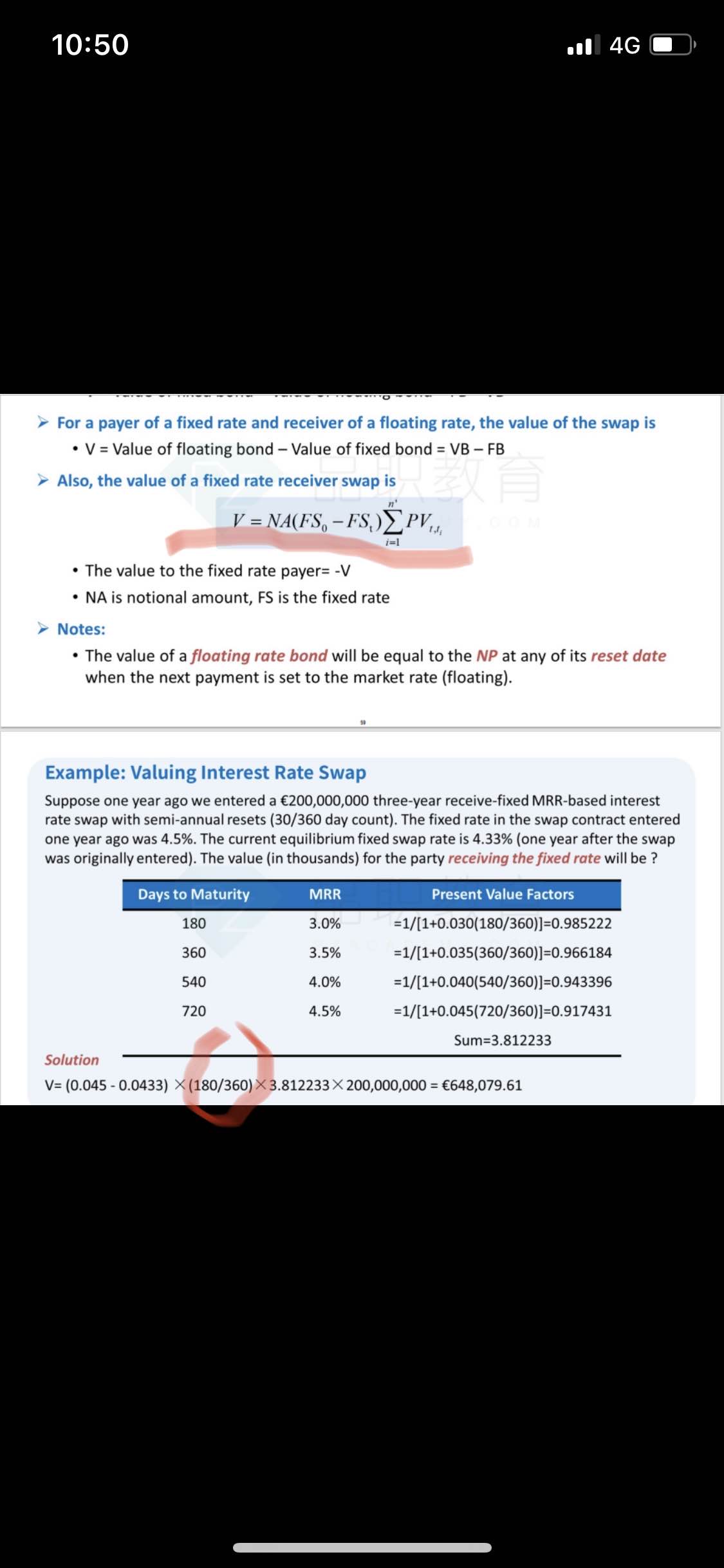

Suppose one year ago we entered a

€200,000,000 three-year receive-fixed Libor-based interest rate swap with

semi-annual resets (30/360 day count). The fixed rate in the swap contract

entered one year ago was 4.5%. The value for the party receiving the fixed rate

is:

选项:

A.- €648,079.61

B.

€648,079.61

C.

- €548,068.57

解释:

B is correct

本题考察的是利率互换求value。

先求出在t=1时刻的互换的固定利率:

fixed swap rate = (1- 0.917431) / 3.812233=2.1659%

annulized: 2.1659% * 360/180 = 4.3318%

然后计算value,对于fixed receiver:

V= (0.045 - 0.0433)

×(180/360)×3.812233×200,000,000 = €648,079.61

这个公式哪一项里体现出来要乘个180/360了?