NO.PZ2022062601000016

问题如下:

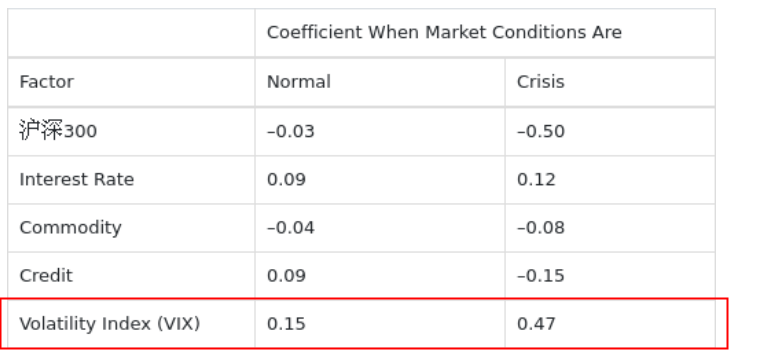

Fund A invests in many different hedge fund strategies. The factor sensitivities for Fund A during normal conditions and crisis conditions are highlighted in Exhibit 1. At the 5% level, all exposures are significant.

Exhibit 1.

Fund A Coefficients

选项:

A.

Observation 1

B.

Observation 2

C.

Observation 3

解释:

C is correct. For Fund A, adding deep out-of-the-money puts during periods of market stress would explain why the correlation with equity markets is relatively neutral in normal markets but is significantly negative during periods of crisis. It also is supported by a large increase in positive correlation with volatility during periods of crisis.

A is incorrect. Fund A is unlikely to have a dedicated short bias strategy, as its sensitivity to the equity market is essentially zero except during crisis periods.

B is not correct. Fund A has a positive exposure to volatility through the VIX, especially during periods of market pressure. This does not mean that managers will sell puts against short positions.

知识点考察:Portfolio Contribution of Hedge Fund Strategies

A选项,dedicated short bias是指完全做空,那么其和沪深300的系数值应该是负的。虽然normal的时候是是负的,但是-0.03,基本等于没有,所以与其说是dedicated short bias感觉更想EMN。所以A不对。

B选项。说是卖出期权。期权和波动率是正比,这时如果卖出期权,那么就是和波动是反比。crisis时期是高波动的,那么应该系数是小的,但是CRISIS的时候VIX的波动是增加的。所以不对。

C选项,其描述简单是说持有PUT,也就是option,还是和B解题思路一样。PUT是option,与波动成正比,CRISIS的时候是高波动,所以这个时候应该系数是增加的。而表格的VIX的crisis比normal高(0.47>0.15),所以证明C是对的

完全没有看懂这道题目,老师能给讲解一下吗?