NO.PZ2023091802000120

问题如下:

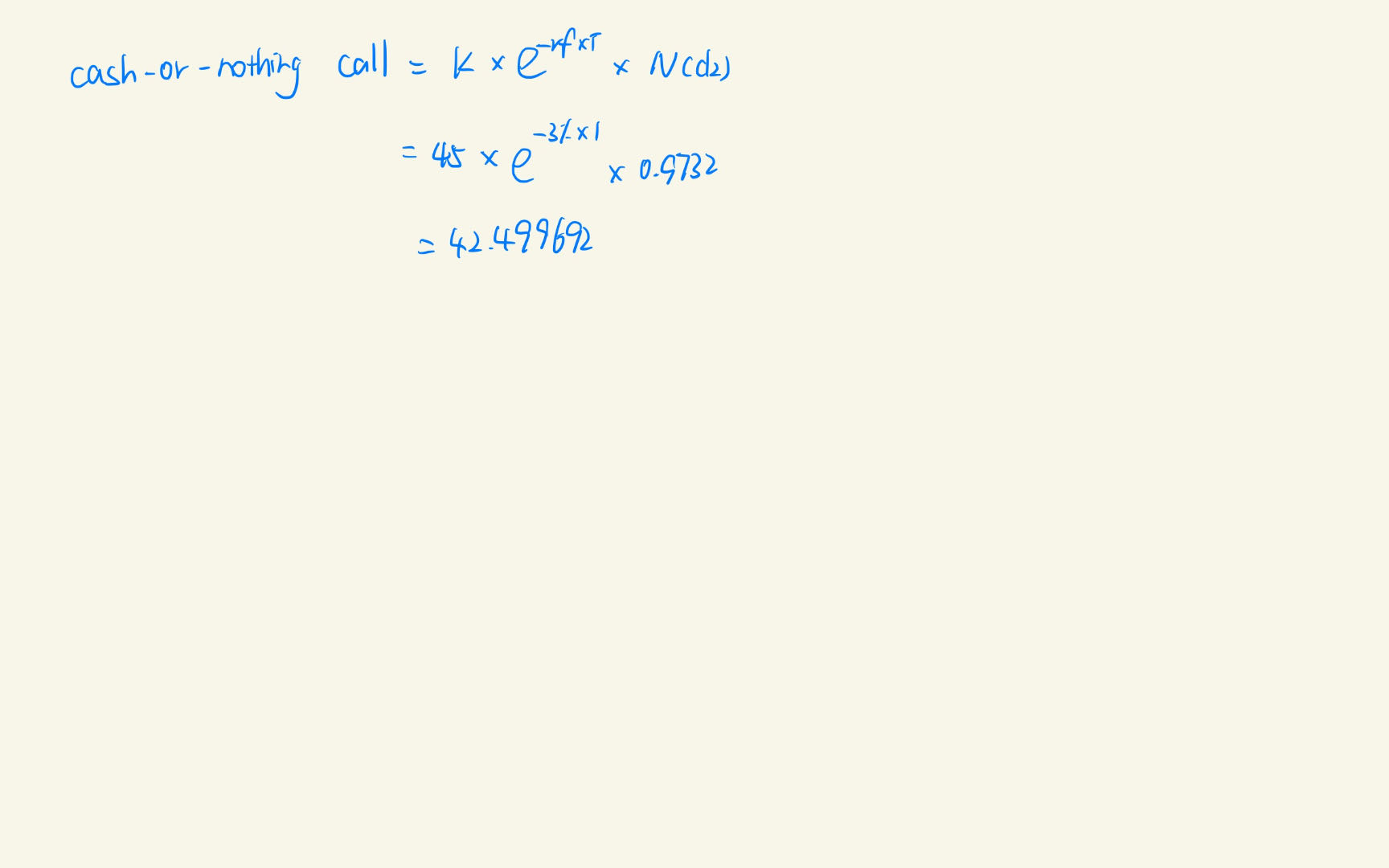

A cash-or-nothing call (also known as a digital call) pays a fixed amount to the buyer if the asset finishes above the strike price. Assume that at the end of a 1-year investment horizon, the stock is equal to $50, the fixed payment amount is equal to $45, and N(d1) and N(d2) from the Black-Scholes-Merton model are equal to 0.9767 and 0.9732, respectively. The value of this cash-or-nothing call when the risk-free rate equals 3% is closest to:

选项:

A.$5

B.$42

C.$44

D.$47

解释:

请解释一下这题,谢谢!