NO.PZ2022062760000027

问题如下:

The recent performance of Prudent Fund, with USD 50 million in assets, has been weak and the institutional

sales group is recommending that it be merged with Aggressive Fund, a USD 200 million fund. The returns on

Prudent Fund are normally distributed with a mean of 3% and a standard deviation of 7%, and the returns on

Aggressive Fund are normally distributed with a mean of 7% and a standard deviation of 15%. Senior

management has asked an analyst to estimate the likelihood that returns on the combined portfolio will

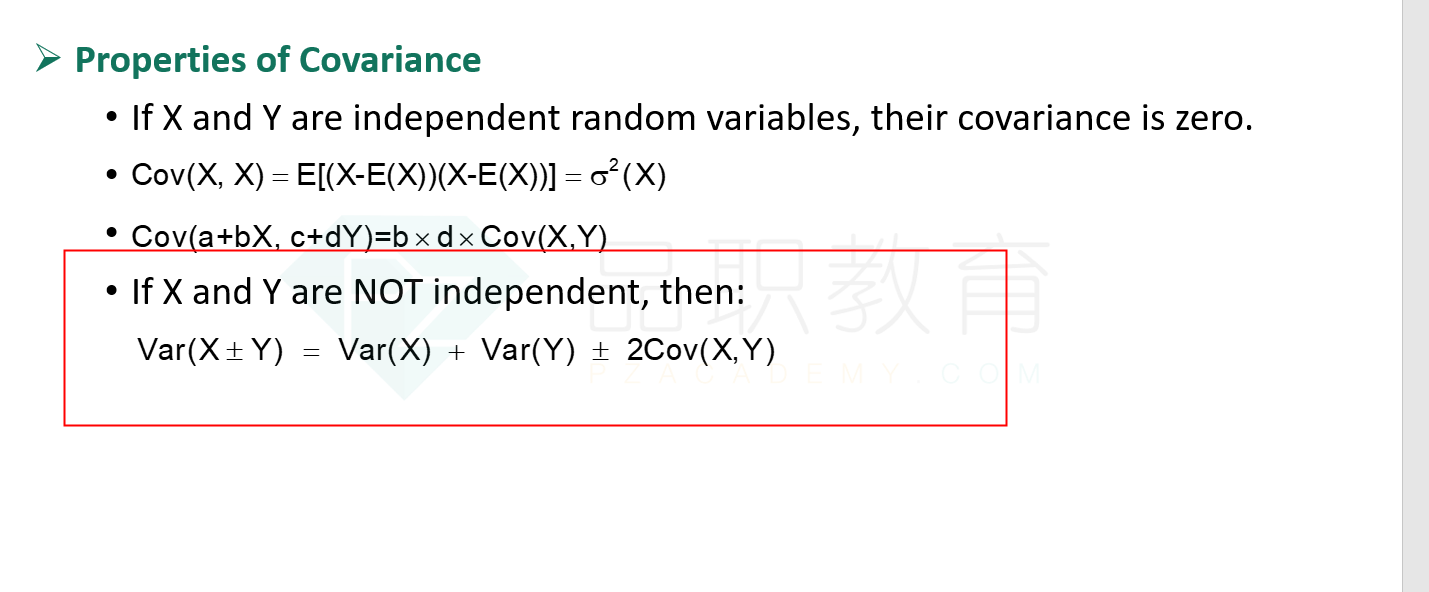

exceed 26%. Assuming the returns on the two funds are independent, the analyst’s estimate for the

probability that the returns on the combined fund will exceed 26% is closest to:

选项:

A.

1%

B.

2.5%

C.

5%

D.

10%

解释:

中文解析:

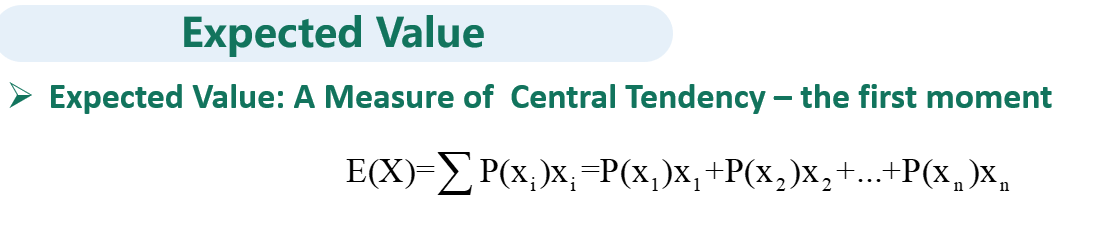

首先计算均值:

𝜇 = 0.2 ∗ 3% + 0.8 ∗ 7% = 6.2%

然后计算σ:

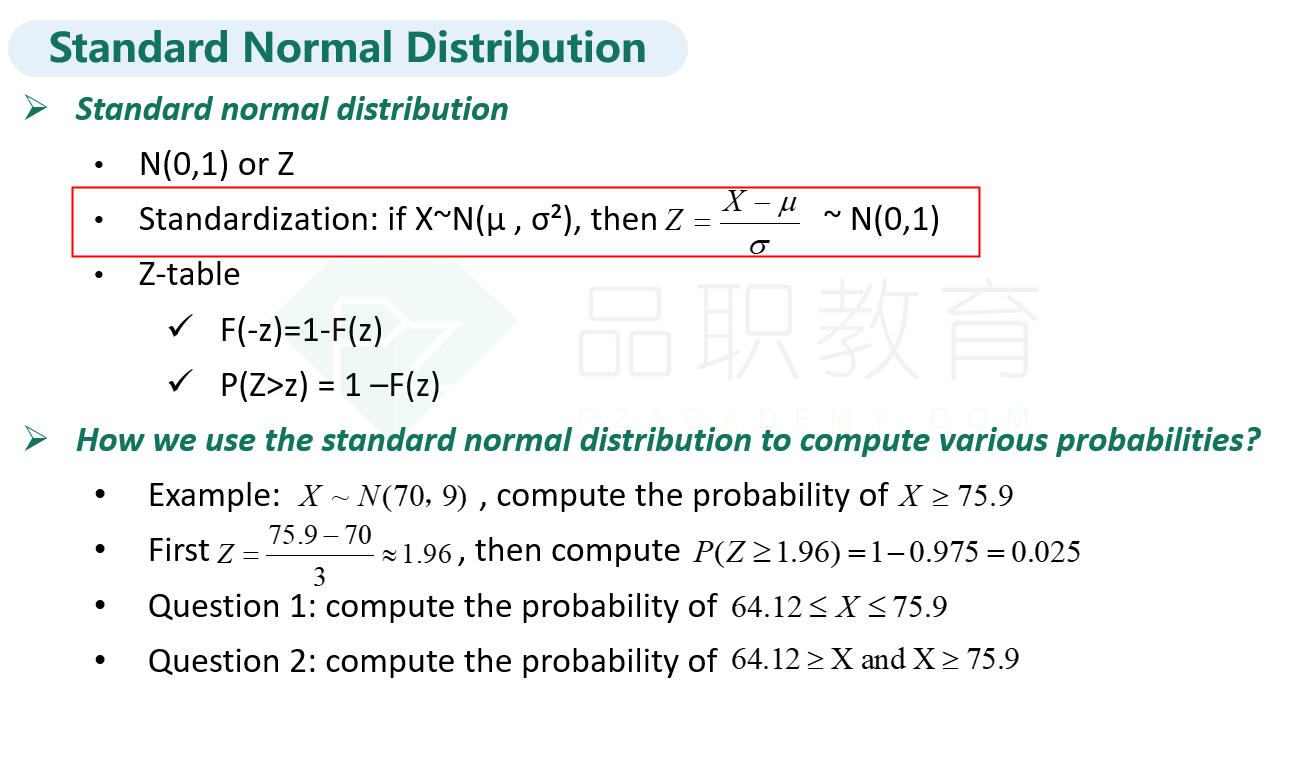

标准化之后的z值=

因此𝑃(𝑍 > 1.64) = 1 − 0.95 = 0.05 = 5.0%

选C

Since these are independent normally distributed random variables, the combined expected mean return is:

𝜇 = 0.2 ∗ 3% + 0.8 ∗ 7% = 6.2%

Combined volatility is:

The appropriate Z-statistic is:

Therefore, 𝑃(𝑍 > 1.64) = 1 − 0.95 = 0.05 = 5.0%

这道题用什么公式呢?